Borderless Retirement: Strategic Positioning of U.S. Social Security in Japan (2026 Edition)

By Aki | Navigator Japan

For Americans retiring in Japan, U.S. Social Security is not just a monthly pension payment. Where you receive it, how you report it, and how Japan treats it for tax and inheritance purposes can materially affect your retirement strategy.

While the process is straightforward for some, others face administrative hurdles that can delay payments. This article shares strategic positioning based on hard-won lessons to help you protect and manage these benefits as a high-value asset in 2026.

Quick Summary

Table of Contents

2026 Landscape: Navigating Administrative Volatility

Strategic Mapping: Identify Your Eligibility Profile

Technical Engine: Qualification Rules & The Treaty Bridge

How and where you receive payments: USD vs. JPY

Survivor Benefits: Inheritance Tax Trap

Navigator’s Action Plan (Checklist)

Q&A

Wrap Up

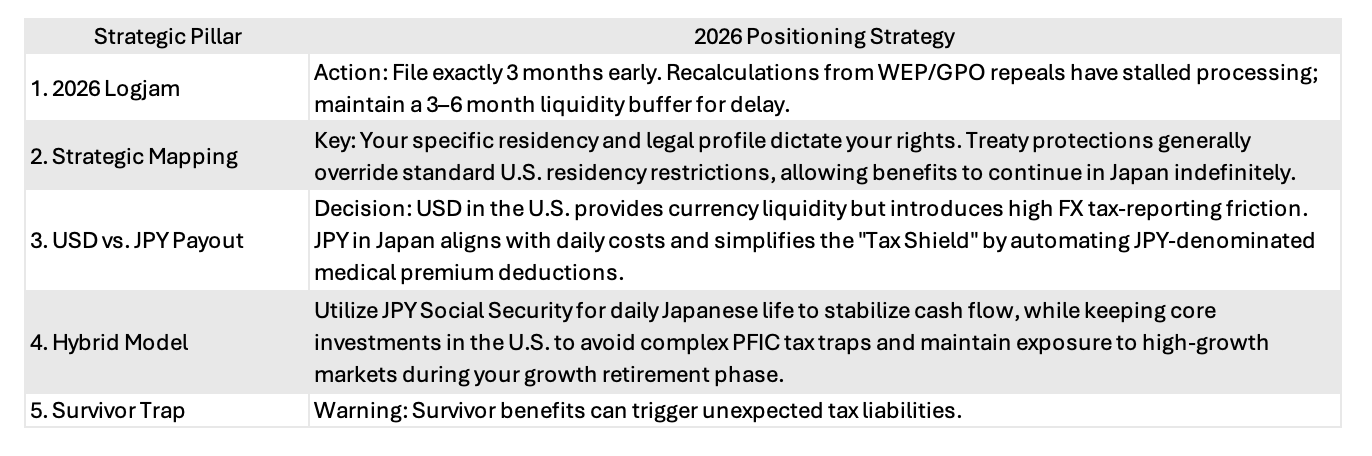

1. 2026 Landscape: Navigating Administrative Volatility

If you applied for benefits in early 2026 and have yet to see a deposit, you are navigating a unique historical logjam.

Administrative Backlog: Following the 2025 repeal of the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO), the Social Security Administration (SSA) began manually recalculating millions of records involving foreign pensions. Although retroactive payments began in February 2025, the complexity of international cases continues to delay processing for applicants in Japan.

Case Study (The Delay in Practice): Recent applications highlight this volatility. In one instance, a resident in Japan applied 3 months prior to her December birthday in 2025. Despite completing interviews and receiving a final calculation by December, the deposit failed to arrive in February 2026.

Upon inquiry, the Tokyo Federal Benefits Unit (FBU) required a second final confirmation including spouse benefit, extending the wait by another 3 months. She has been still waiting as of May 1, 2026.

Strategic Move: Maintain 3–6 Months of Liquidity. Because target deposit dates are currently unreliable, you must maintain a cash buffer to manage processing volatility.

Back Pay Rule: Your funds are protected. Payments are anchored to your Entitlement Date (資格発生日) rather than the date of administrative approval. Once the manual recalculation is finalized, you will receive a single lump-sum deposit covering all benefits owed from your original eligibility date.

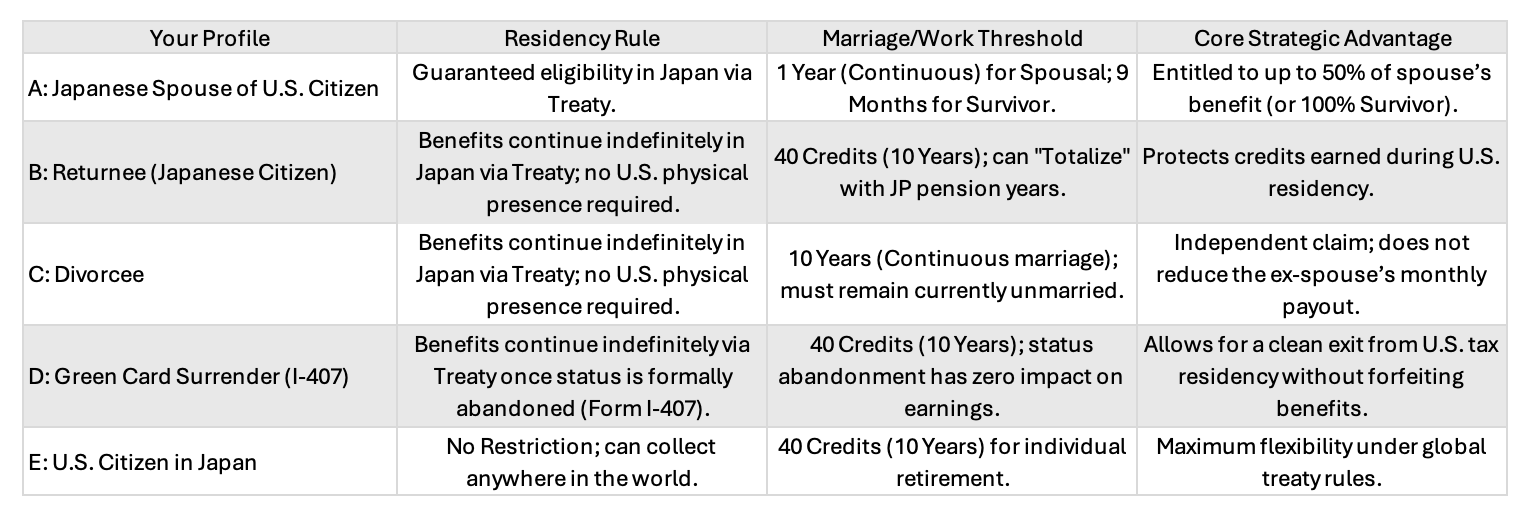

2. Strategic Mapping: Identify Your Eligibility Profile

Before navigating the technical requirements, you must first identify which treaty-protected framework governs your specific residency and marital history.

Note on Citizenship: Changing your nationality from American to Japanese has zero impact on your earned Social Security eligibility.

While this matrix identifies your primary eligibility, the critical age thresholds, residency exceptions, and payout architectures are detailed in the following sections.

As for suvivors, see Section 5.

3. Technical Engine: Qualification Rules & The Treaty Bridge

Understanding the "Engine" means knowing the mechanical rules that trigger your payment. While the U.S. system has strict defaults, the U.S.-Japan Social Security Treaty acts as a bridge to override them.

40-Credit Standard (10-Year Rule): To qualify for Social Security benefits, you typically need 40 "credits" (approximately 10 years of work). However, the Treaty allows for Totalization: if you lack enough U.S. credits, you can "import" Japanese pension years to meet the 40-credit eligibility threshold.

Pro-Rata Adjustment (Payout Reality): While Japanese work years help you qualify for a check, they do not increase the amount of that check. The SSA calculates your "Partial Benefit" by prorating the amount based strictly on your actual U.S. earnings history; totalization simply opens the door to receiving that fraction of the benefit.

6-Credit Floor: Totalization has a limit. You must have earned a minimum of 6 U.S. credits (roughly 1.5 years of U.S. work) for the Treaty to be activated. If you have fewer than 6, you cannot claim U.S. benefits regardless of your Japanese history.

6-Month Myth (Residency Protection): Standard U.S. law stops payments to non-citizens who live outside the U.S. for more than six months. Japanese citizens in Japan are specifically exempt from this rule via the Treaty, allowing for a permanent and legal return to Japan without loss of income.

To maintain this exemption, you must proactively update your administrative record with the Tokyo Federal Benefits Unit (FBU) to ensure your Japanese address is officially on file.

Age Thresholds (Cost of Early Payouts): While you can technically begin receiving reduced benefits as early as age 62, your Full Retirement Age (FRA)—the age at which you receive 100% of your benefit—is determined by your birth year (usually age 67 for those retiring now). Claiming at 62 results in a permanent monthly reduction.

3-Month Filing Window: You are eligible to file your application exactly three months prior to your Month of Entitlement (typically the month of your 62nd birthday or Full Retirement Age).

While the SSA technically allows this lead time, the 2026 administrative logjams make it a strategic necessity to file at the earliest possible date. Filing precisely at the 90-day mark ensures your "Entitlement Date" is locked in, even if the actual administrative approval takes several additional months.

4. How and where you receive payments: USD vs. JPY

With the JPY fluctuating near JPY160 per USD in 2026, the mechanics of how you receive your benefit—and how it is eroded by taxes and insurance—is a critical decision. To make an informed choice, you must look beyond surface-level income tax and evaluate the Total Factors of Erosion.

Structural Comparison: How Your Benefit is Eroded

The debate over whether it is better to receive U.S. Social Security in the U.S. or Japan is often distorted by unrealistic scenarios, such as assuming zero investment income or residency in a tax-free state like Florida . In reality, the burden is simply structured differently.

USD Pathway/Bank Deposit in the U.S.: Variable Risk Model

Income -Triggered Taxation (Combined Income Formula): U.S. Federal tax is highly suppressed only if Social Security is your sole income. Once "Combined Income" (including 401(k) draws, dividends, or rent) exceeds specific thresholds (USD25k–USD34k), it triggers taxation on up to 85% of your benefit.

Notably, this refers to the portion added to your taxable income, not your actual tax rate, which remains tied to your standard marginal bracket.

Medical Volatility (The Privatized Risk): While U.S. taxes may appear lower, healthcare is privatized and less predictable. Medicare generally does not cover treatment in Japan.

Yet many retirees continue paying Medicare Part B premiums to avoid permanent late-enrollment penalties and preserve future access to the U.S. healthcare system. This can create a “double premium” burden for Japan residents already covered under Japan’s mandatory National Health Insurance system.

JPY Pathway/Bank Deposit in Japan: Fixed Comprehensive Model

Progressive Visibility: Japan taxes U.S. benefits as Miscellaneous Income. At a 2026 exchange rate of 160, a high-value benefit of USD 4,500 per month (approx. JPY 7.2M) naturally lands in a 20–25% bracket for the combined burden of Income Tax, Resident Tax, and Social Insurance (Health/Long-Term Care).

Fixed Obligation: Regardless of payout location, Japanese residency (3+ months) triggers mandatory enrollment in National Health Insurance.

Year 1 Reality: Unlike foreign investment dividends, which may enjoy a 5-year remittance-based deferral for Non-Permanent Residents, U.S. Social Security is taxable in Japan from Year 1.

System Value (Why you pay): While mandatory, your premiums unlock the High-Cost Medical Expense Benefit (高額療養費制度)—an income-based ceiling on monthly out-of-pocket exposure—and Long-Term Care Insurance, which provides robust home-based care systems often unavailable in the U.S..

Strategic Mitigation: Optimizing the Japanese Footprint

While the burden is visible, it can be optimized through several realistic levers:

Income Control: Dispersing other income (dividends/gains) across different years can prevent jumping into higher tax brackets .

Deduction Maximization: Utilize basic, spouse, and medical expense deductions, including insurance premiums such as earthquake, and senior care costs to lower the taxable base .

Operational Strategy: Pathways to Receipt

Option 1: Direct Deposit in Japan (JPY)

o Advantage: The SSA converts USD to JPY using a specialized treaty rate with no FX transaction fees.

o Efficiency: This provides a clean tax trail for Japanese tax returns.

Option 2: U.S. Bank Deposit (USD)

o Advantage: Retaining benefits in USD may help offset JPY weakness and support U.S.-based expenses.

o Administrative Burden: You are legally required to track and report Foreign Exchange Gains if you convert to JPY at a rate higher than the receipt-date rate.

Navigator’s Recommendation

For most retirees in Japan, receiving Social Security Benefits payment in JPY directly to a Japanese bank is the superior structural choice.

Liquidity Alignment: It aligns your cash flow with your JPY-denominated cost of living.

Tax Shield Optimization: While you pay National Health Insurance and Long term Care Insurance premiums via invoice, receiving JPY simplifies the reconciliation during your Final Tax Return. Proactively reporting these 100% deductible premiums is the way to lower your Resident Tax footprint.

Zero FX Accounting: You bypass the complex "Miscellaneous Income" reporting required for foreign exchange gains that occur when shifting USD into Japan for monthly expenses.

Navigator’s Pivot: Legacy planning is a concurrent track. Review your assets in advance and decide where they should be held and managed to reduce future legal and tax complexity across countries.

Age of Entitlement Action Plan

As you reach the age of entitlement, your strategic plan must prioritize the following three pillars:

Tax Explainability: Maintain a rigorous compliance trail (cost basis, liquidation dates, and 401(k) logs). Precise documentation is your primary defense in justifying "Miscellaneous Income" and capital gains for tax return.

Jurisdictional Architecture: Adopt a "Hybrid Model" for efficiency: utilize JPY-denominated Social Security for daily Japanese living expenses while maintaining U.S.-based investments to bypass complex Japanese PFIC tax complications.

Administrative Precision: Standardize your name string across your Passport, SSA record, and Japanese bank account. Perfect alignment (including middle names) is mandatory to prevent catastrophic deposit failures and multi-month administrative logjams.

5. Survivor Benefits: Inheritance Tax Trap

A critical 2026 development is the Tokyo District Court ruling (Feb 25, 2026), which confirmed that the right to receive U.S. survivor benefits constitutes “Deemed Inheritance” (みなし相続財産).

If the decedent is a U.S. citizen and the beneficiary is a resident of Japan, the capitalized value of future survivor benefits are subject to Japanese inheritance tax, regardless of the recipient’s citizenship or Green Card status.

Deemed Inheritance Ruling

In practice, Japanese tax authorities calculate the present value of these future payments based on the recipient's projected life expectancy. This creates a phantom asset that can push an estate over the tax-free threshold before a single dollar is ever received.

Strategic Defense: Utilizing Exemptions

To mitigate this liability, you must proactively apply the Japanese Spouse Exemption. This shields the higher of:

JPY160 Million, OR

Spouse’s Statutory Inheritable Share (法定相続分相当額).

Important: The spouse’s Statutory Inheritance Share is determined by Japanese law and exists independently of any Will or Estate Division Agreement. However, a valid Will or formal Estate Division Agreement remains essential for the actual allocation of assets.

Eligibility & The Totalization Treaty

Survivor Threshold: To unlock Treaty benefits on a decedent's record (if they had fewer than 40 credits), the worker must have earned at least 6 U.S. credits (approx. 1.5 years).

9-Month Rule & Accident Waiver: Survivors generally require a 9-month marriage duration. However,this is waived for accidental deaths, ensuring immediate eligibility regardless of marriage length.

Age 60 Floor: Standard survivor payments begin at age 60. The only path to receiving benefits earlier (regardless of cause of death) is if the survivor is caring for the decedent's child (under 16 or disabled).

6. Navigator’s Action Plan (Checklist)

As you reach the age of entitlement, transition from waiting to positioning by completing these five administrative pillars:

1. [ ] Eligibility Mapping: Formally verify your "Category" (Individual, Spousal, or Totalized) and confirm your primary benefit amount. Do not rely on estimates more than 12 months old.

2. [ ] Character Match Audit: Confirm your name string is an identical match across your Passport, SSA Record, and Japanese Bank Account. In Japan’s banking system, a missing middle name or a hyphenation discrepancy can trigger a year-long deposit bounce.

3. [ ] USD or JPY Election: Finalize your choice between USD (Strategic Liquidity) or JPY (Operational Efficiency). Remember: Japanese taxing rights apply from Year 1 regardless of your choice; ensure your "Tax Trail" is ready for the NTA.

4. [ ] 3-Month Filing Window: Initiate your application exactly three months before your target start date. The 2026 administrative logjam means last-minute filings risk significant liquidity gaps.

5. [ ] Tax Explainability: Maintain a compliance trail (cost basis and withdrawal logs) for all U.S. and Japanese assets to justify Miscellaneous Income and capital gains for tax return.

6. [ ] Jurisdictional Architecture: Adopt a "Hybrid Model" for cash flow. Use direct JPY Social Security deposits for daily costs in Japan while keeping core investments in the U.S. to minimize Japanese PFIC complications.

7. [ ] Administrative Precision: Simplify your account footprint and ensure exact name-string redundancy across all institutions to prevent catastrophic deposit failures or multi-month administrative logjams.

7.Q&A

Q1: Can I receive U.S. Social Security while living in Japan?

A1: Yes. Under the U.S.-Japan Social Security Totalization Agreement, eligible recipients can generally continue receiving benefits while residing in Japan.

Q2: Is U.S. Social Security taxable in Japan?

A2: Yes. For Japanese residents, U.S. Social Security benefits are treated as Miscellaneous Income and are taxable in Japan.

Q3: Does Medicare cover medical treatment in Japan?

A3: Generally, no. Medicare typically does not cover routine medical treatment received outside the United States, including in Japan.

Q4: Are U.S. survivor benefits subject to Japanese inheritance tax?

A4: Yes. A 2026 Tokyo District Court ruling recognized certain U.S. survivor benefits as “Deemed Inheritance Assets,” meaning their capitalized value is currently treated as subject to Japanese inheritance tax for residents of Japan.

8.Wrap Up

U.S. Social Security is not a set-and-forget benefit. It is a dynamic asset that requires jurisdictional precision.

While most of us are too busy to manage the intricacies of cross-border systems, the administrative and tax risks are real. To avoid costly surprises—from deposit failures to phantom inheritance taxes—the key is to move from passive waiting to active positioning. Plan ahead, verify your data, and secure your take-home value.

Disclaimer: This guide is based on 2026 regulations and recent judicial rulings. Because individual financial circumstances, residency histories, and family structures vary significantly, these strategies may not apply universally. Always consult qualified tax and legal professionals regarding financial planning, estate planning, and tax filing obligations.

Aki | Japanese | Former Head of HR in Global Finance

Aki has served as Head of Human Resources in the global financial sector. With over two decades of experience navigating labor law, residency, and wealth protection in both Tokyo and Chicago, she now provides the "insider’s roadmap" for foreigners planning a stable, high-value long-term life and retirement in Japan.