Premium Care Roadmap: Navigating Quality and Optionality in Japanese Senior Living

By Aki | Navigator Japan

For many international residents, the dream of “aging in place” is the ultimate goal. To achieve this, we build a “Home Care Collective” and leverage Japan’s Long-Term Care Insurance (LTCI) system.

Note: If you haven’t yet established your home-base strategy, start here:

Home Care Collective: A Case Study in Architecting Senior Support in Japan

However, the ultimate goal of this preparation isn't just to "stay home"—it is to maintain Optionality.

Make thoughtful use of Japan’s infrastructure to help preserve your capital—so that, even in times of uncertainty, you remain in control.

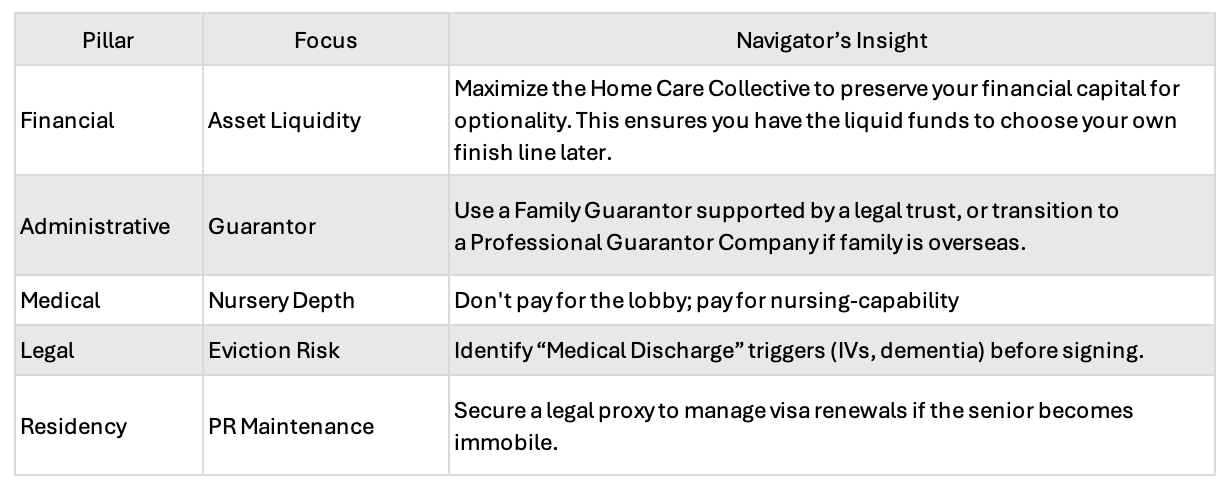

Quick Summary: 5 Pillars of Optionality

Senior care in Japan is a Horizontal Impact event where a shift in one domain creates a ripple effect across all others.

Table of Contents:

1. Strategy: Why “Home First” is a Financial and Personal Hedge

2. Administrative Horizontal: Solving the Guarantor Wall

3. Medical Horizontal: Securing Your Medical Depth

4. Financial Vertical: Asset Liquidity & Depreciation

5. Geography vs. Language: Mother Tongue Trap

6. Q&A

7. Wrap up

1. Strategy: Why “Home First” is a Financial and Personal Hedge

The Japanese government’s "Aging in Place" policy is a strategic opportunity. By utilizing the Home Care Collective—a subsidized infrastructure of visiting nurses, helpers, and rehab specialists—you avoid the "middle-ground waste" common in uncoordinated systems.

The Logic of Subsidized Stability

Leveraging Japan’s Long-Term Care Insurance (LTCI) creates a phase where users pay only 10%–30% of care costs. This is a sophisticated Capital Preservation Strategy:

Avoid the Freedom Penalty: Moving to a facility too early trades your autonomy for unnecessary oversight. Remaining home maintains your dignity, familiarity, and social independence.

Prevent Asset Erosion: Premium facilities carry a high monthly burn rate. Every month managed at home protects the liquidity of your Optionality Fund.

Compound Your Gains: Affordable, subsidized care allows your core investments to grow. This ensures that if a medical move becomes mandatory, you have the maximum capital to afford a top-tier choice.

Manage the Benefit Ceiling: LTCI subsidies have a monthly cap based on your care level.

Example: As of April 2026, the ceiling for Level 1 care (Yokaigo 1) is approximately 16,765 units (JPY167,650) per month. Any services beyond this limit are paid at 100% out-of-pocket.

Even so, the "Home Care Collective" remains significantly more cost-effective than the high fixed costs of early facility entry.

Real Story: USD50/Hour Companion Trap

In 2016, my husband’s family in Illinois hired private help for an aunt at USD50 per hour. Despite the cost, contractual limits prevented the helper from cooking, cleaning, or providing clinical oversight. We were paying for a safety companion while medical risks remained unmanaged. This inefficiency eventually forced a move to a nursing home.

Clinical Threshold: Designing Your Finish Line

The goal of the Home Care Collective is to protect your assets during the manageable years so that when you hit the Clinical Limit—the point where safety or medical needs exceed home capacity—you have the Optionality to choose your transition:

Premium Move: A high-end Nursing-care facility with 24/7 on-site clinical depth and English-ready infrastructure.

Intensive Home Hospice: Utilizing preserved liquidity to hire private, 24/7 medical staffing to support in your own residence. Note: While this preserves familiarity, family involvement is inevitable.

Navigator’s Take: Stay home as long as support allows. You gain the autonomy of familiarity while the government effectively subsidizes the preservation of your capital.

2. Administrative Horizontal: Solving the Guarantor Wall

For international residents, the highest barrier to entry for premium facilities is not the admission fee—it is the Guarantor (Mimoto Hosho) system. In Japan, a guarantor is a local proxy responsible for three critical horizontal pillars:

Financial Indemnity: Joint liability for all costs and potential damages.

Daily Life Support: Accompaniment and assistance with daily activities, including hospital visits, shopping, and outings.

Post-Mortem Logistics: Handling body claiming, room clearing, and final arrangements.

Solution: Specialized Senior Life Guarantors

If your primary family resides in London or New York, they cannot effectively manage these local, time-sensitive duties. The solution is a Specialized Senior Life Guarantor (身元保証会社).

These firms function as your "Professional Family." However, costs and service structures vary significantly between providers (including initial fees, monthly retainers, and deposits).

While service structures vary, expect a market range of JPY 1M – JPY 2M (approx. USD 6.3K – 12.6K). This typically covers the basic entry-level contract plus common options such as emergency call handling, administrative support, and final arrangement prep. Depending on the resident's health condition, additional monthly fees may apply for daily living support.

To manage this risk of cost and services, obtain quotes from at least three firms and evaluate them based on:

Scope of Coverage: Do they provide emergency 24/7 response and hospital accompaniment?

Deposit Security: What are the specific refund conditions for unspent deposits?

Facility Partnerships: Does the firm have a pre-existing relationship with your target facility?

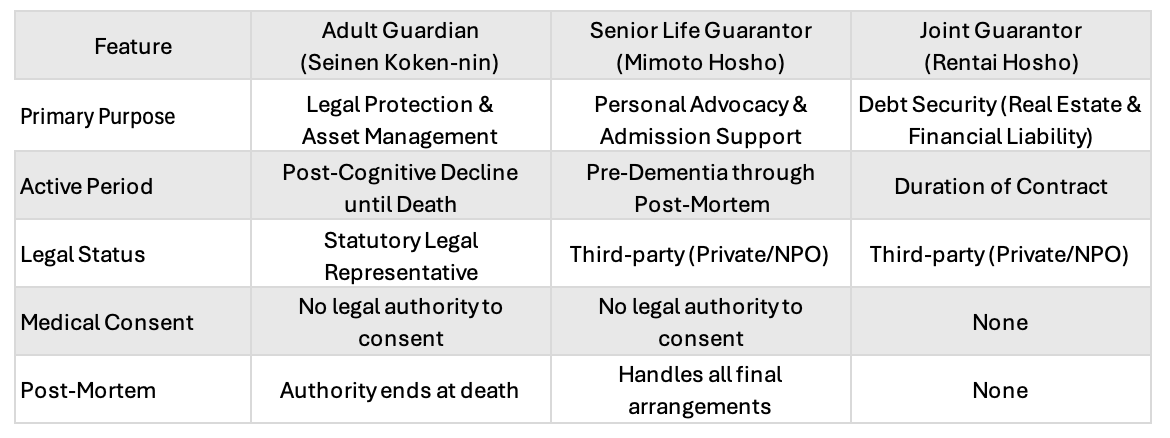

Defining the Boundaries: Who Does What?

It is vital to distinguish between three roles that are often confused by foreigners, as they have different legal authorities:

Critical Nuance: Medical Consent Void

A major misconception is that a Guarantor or Guardian can legally "sign off" on surgery or end-of-life care —but they cannot.

Legal Restriction: Medical consent is a personal right. No third party—even a legal guardian—has definitive legal authority to consent to treatment if the patient lacks capacity.

Navigator’s Move: To bridge this gap, you must proactively document your preferences through an Advance Directive (Jizen Shiji-sho) while you have full capacity. While these lack absolute legal binding power in Japan, they serve as the essential foundation for Advance Care Planning (ACP)—the consensus-based model where medical teams and families align on your desired care. Without this document, you risk a "decision void" where your personal values are sidelined during a crisis.

Guardian Conflict

An Adult Guardian cannot act as your guarantor due to a fundamental legal conflict of interest. Because a Guardian’s primary duty is to protect your assets while a guarantor’s duty is to pay your creditors, they cannot legally fulfill both roles.

Risk Mitigation: Transparency Gap

The guarantor industry lacks standardization. Misalignments between verbal promises and contract clauses are common.

Documentation Shield: Maintain a navigator file of all original contracts, historical quotes, and meeting memos.

Public Safety Nets: If a dispute arises over fees or service, contact the Consumer Affairs Agency (CAA) for contract mediation or your local Community General Support Center to evaluate if service failures are jeopardizing your care.

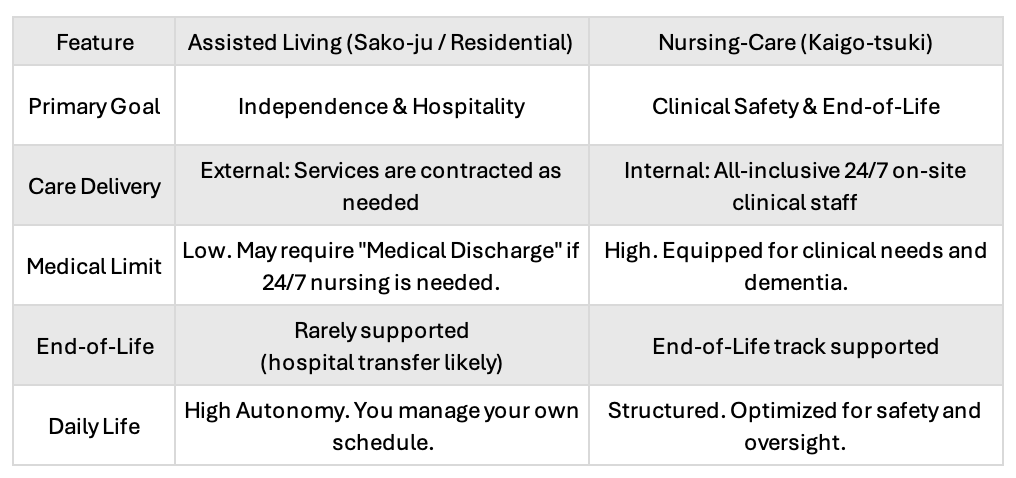

3. Medical Horizontal: Securing Your Medical Depth

When touring good facilities, it is easy to be charmed by the architecture. However, the true value of a facility lies in its Medical Depth. In Japan, there is a distinct horizontal divide between lifestyle-focused residences and clinical-ready homes.

Navigator’s Strategy: Strategic Transition

The objective is to maximize your independence at home via the LTCI system, then transition to high-depth Nursing Care for the final chapter. We recognize the psychological weight of this move. Leaving a long-time residence to "start over" is a valid emotional hurdle. However, by preserving your capital early, you are securing a Medical Fortress.

Navigator’s Reality Check: Public vs. Commercial

While this guide focuses on Commercial (Private) facilities for their immediate availability and premium standards, Japan also offers Public nursing homes. However, for the international professionals, these are rarely a strategic priority due to high occupancy and multi-year waiting lists. Your "Home First" strategy is designed to build the liquidity required to bypass these queues and access the private market on your own terms.

4. Financial Vertical: Asset Liquidity & Depreciation

In Tokyo, a premium facility move is a major investment. Admission fees of JPY10M to JPY22M are standard. However, as a risk manager, you must look at the Amortization Schedule.

Refund Policy: Most deposits "depreciate" over 5 to 7 years. If your parent passes away 18 months after moving in, a significant portion of that deposit should be refunded to the heirs. You must verify the Initial Depreciation percentage (often 10–30%).

Monthly Burn Rate: Beyond the admission fee, monthly costs in premium urban hubs frequently exceed JPY 300k–500k. This burn rate combines fixed expenses—such as rent equivalents, management fees, and meal plans—with variable costs like medical expenses, hygiene supplies, and personalized assistance.

Account Freeze Risk: Banks lock accounts once they become aware that a client has lost mental capacity. While many families unofficially may use a parent’s cash card, this is a security violation and a fragile workaround. If the card is lost or the bank detects third-party activity, your access to the senior’s funds vanishes instantly. You must establish a Bank-Registered Proxy (Dairinin), a Family Trust, or a Legal Guardian while mental capacity is high.

See also Will Your Accounts Freeze? Navigating Cognitive Decline & Banking in Japan [2026 Guide]

5. Geography vs. Language: Mother Tongue Trap

Choosing a location is a trade-off between capital preservation and Communication Infrastructure.

Rural Paradox: Regional facilities offer lower costs, shorter waiting lists, and access to Japan's natural landscapes. However, this serenity often comes with a language Lockup. While medical care is excellent, a lack of English-speaking staff creates a functional barrier; a resident cannot accurately describe pain or symptoms, compromising the efficacy of their care.

Urban Premium: Major hubs like Tokyo,Osaka, or Kanto area provide a safety net against Dementia Language Reversion—the medical phenomenon where bilingual seniors lose their second language and revert to their mother tongue. These cities host the highest density of English-capable medical professionals.

Silver Lining: Leveraging International Staff

Japan’s care sector now includes 90,000 foreign staff (primarily from Indonesia, Philippines, and Myanmar). Often university-educated with nursing backgrounds, these English-proficient caregivers are concentrated in urban centers, offering a vital horizontal safety net for non-Japanese speakers.

See also Senior Care in Japan: Costs, Choices, and What Foreigners Should Know

📋 Facility Audit: 5 Critical Questions

Ask these five questions to see if a facility can actually support your Optionality:

[ ] Eviction Trigger: What specific clinical conditions (e.g., feeding tubes or behavioral dementia) mandate an immediate discharge?

[ ] Nursing Ratio: Is a registered nurse on-site 24/7, or merely on-call?

[ ] Amortization Clock: What is the exact refund schedule for the admission fee if a resident passes away within the first 6 months?

[ ] Language Buffer: What specific tools or staff training are in place for residents who can no longer communicate in Japanese?

[ ]. End-of-life care: Does the facility have a formal partnership with a hospital to provide 24/7 end-of-life care on-site?

6. Q&A

Q1: Can I hire a private English-speaking helper to work inside a Japanese facility?

A2: Usually, no. Most Nursing-care facilities are all-inclusive. Bringing in an outside helper creates liability and insurance conflicts. You must choose a facility that already has the language and medical depth you need.

Q2: What happens to my parent's Permanent Residency (PR) if their mental capability declined?

A2: Permanent Residency itself does not expire and does not require renewal. However, the Residence Card must be renewed every 7 years. If your parent is unable to appear in person due to conditions such as dementia or a coma, a family member or authorized representative can apply on their behalf.

7. Wrap-up: The Cultural Threshold

In the West, transitioning to a facility is often a last resort to preserve autonomy. In Japan, however, the priority is safety and longevity; many move into assisted living early to proactively secure their future.

Navigator’s Reality: My father remains at home via LTCI support—a choice only possible because he maintains a clear mind and uses a walker to stay mobile. Observing him has taught me that the "Home First" phase requires a daily commitment to physical activity. To avoid becoming bedridden, the effort to stay walking is the most critical hedge we have.

Ultimately, moving to a facility is a strategic pivot. By planning while capacity is high, you ensure your final chapter is defined by your choice, rather than a medical crisis.

Aki | Japanese | Former Head of HR in Global Finance

Aki has served as Head of Human Resources in the global financial sector. With over two decades of experience navigating labor law, residency, and wealth protection in both Tokyo and Chicago, she now provides the "insider’s roadmap" for foreigners planning a stable, high-value long-term life and retirement in Japan.

References

Ministry of Health, Labor and Welfare (MHLW): Guidelines on End-of-Life Care and Advance Care Planning (ACP)

Ministry of Justice (MOJ): Adult Guardianship System Overview (成年後見制度の概要)

MHLW: Advance Care Planning (ACP) – Official Overview Page