International Money Transfers to Japan: Tax & Reporting Risks (2026 Edition)

The "Invitation to the Tax Office"

“Is a money transfer to Japan taxable?” This was my first concern when moving our capital.

The reality: A large wire is a formal disclosure to the tax office. I still remember the stress of watching our life savings sit in "limbo" during a volatile JPY market, fearing a compliance flag would freeze our funds.

While moving your own funds isn't a taxable event, the danger lies in failing to prove the source. This guide provides the structural safeguards to move your capital safely, strategically, and audit-ready.

Quick Summary: Key Takeaways

Invitation Rule: Transfers over JPY 1M are reported to the tax office.

Evidence Folder: Prove the source of funds.

Pre-Clearance: Contact your Japanese bank before large transfers.

Currency Trap: FX gains may become taxable.

5-Year Wall: Global reporting expands after Year 5.

Related article:

How Much to Retire in Japan as an Expat: 2026 Costs, Visas, and Realistic Budgets

Property Titles in Japan: How Cross-Border Couples Can Avoid 2026 Tax & Inheritance Risks

Table of Contents

1. The Evidence Protocol: Defending Your Capital

2. Banking Logistics: The Pre-Clearance Strategy

3. The Currency Trap: Tax on Foreign Exchange Gains

4. The 5-Year Threshold: NPR Status and Foreign Asset Reporting

5. Q&A

6. Wrap-Up: From Risk to Resolution

1. The Evidence Protocol: Defending Your Capital

Any transfer exceeding JPY 1 million triggers an automatic “Overseas Remittance Report” from your bank to the tax authorities.

In some cases, years later, you may receive a formal inquiry letter from the tax office — commonly referred to in Japan as an “O-Tazune” (お尋ね). While not yet a formal tax audit, it is a serious compliance inquiry that should never be handled casually.

Build a “Defense Folder”

Personal Savings:

Bank statements and transaction records showing the gradual accumulation of funds through salary deposits, investments, or other documented income sources.

Investments:

Brokerage statements showing the original purchase cost and the final liquidation of stocks, bonds, or ETFs. This proves the funds are "taxed capital," not "unreported gifts”.

Property Sales:

Final settlement statements (HUD-1 or local equivalent), sale agreements, and supporting tax records showing how the transaction was reported or taxed in the source country.

Gift Defense: Under Japanese law, gifts may legally be established through verbal agreement alone. A formal Gift Contract (贈与契約書) is not mandatory, but documenting the arrangement in writing can become critical during future scrutiny by Japanese tax authorities.

Exchange Rate Record: Retain the exchange rate applied on the date of transfer. This historical record may become important for defending future foreign exchange gain calculations during Japanese tax scrutiny.

O-Tazune (inquiry letter from the tax office): Dangerous Mistakes

O-Tazune often arrives 6 to 24 months after a transfer.

The most common mistakes include:

responding based on vague memory

speculative or inconsistent explanations

statements such as “everyone does this”

Always respond with documentation, not assumptions. If uncertainty exists, verify the records first or consult a qualified tax professional before replying.

2. Banking Logistics: The "Pre-Clearance" Strategy

International money transfers to Japan can be processed through traditional banks, online banks, or service providers such as Wise. The platform itself is not the core issue. The real issue is whether the transaction can survive Japanese compliance review.

A sudden high-value transfer may trigger:

AML (Anti-Money Laundering) review

source-of-funds verification

delayed settlement

returned funds

temporary account restrictions

The "Pre-Clearance" Strategy

For large transfers, proactively contacting the receiving institution before sending funds is an effective risk-management strategy.

Providing supporting documentation in advance may reduce:

compliance delays

additional document requests

rejected transfers

The JPY 30 Million Threshold

Large international transfers trigger Bank of Japan (BOJ) reporting obligations through the receiving financial institution under Japan’s foreign exchange reporting framework.

The Purpose Match

One of the most common operational mistakes is inconsistency in the declared purpose of remittance.

The stated transfer purpose should match:

bank instructions

contracts

property documents

supporting tax records

Examples:

Real Estate Purchase

Family Living Expenses

Capital Transfer

Even small wording discrepancies may trigger additional scrutiny from Japanese banks or tax authorities.

Practical Risk Reduction Tips

Maintain a complete “Evidence Folder” before initiating the transfer.

Keep records showing the origin of funds.

Retain exchange-rate records on the transfer date.

Avoid changing the stated transfer purpose mid-process.

Do not assume Wise or fintech platforms avoid Japanese reporting obligations.

3. The Currency Trap: Tax on Foreign Exchange Gains

One of the most dangerous misconceptions is that moving your own money is always tax-free.

However, the National Tax Agency (NTA) may treat currency conversion as taxable if exchange rate changes increased the value of your foreign currency.

Example

If you earned USD when USD1 = JPY110 and later convert it when USD1 = JPY150, the JPY40 difference per dollar may be treated as a realized FX gain.

The Classification: This is treated as Miscellaneous Income.

The Rate: This gain is added to your other income and taxed at progressive rates. Combined with the 10% Resident Tax, your effective rate could range from 15% to 55%.

CRITICAL NOTE: This tax is triggered by conversion. Moving USD from a US bank to a USD-denominated account in Japan generally does not trigger this gain until the moment you convert it to Yen.

2026 Surveillance

Because the JPY1 million reporting rule (See Section 1) includes the exchange rate at the time of transfer, the NTA has the exact data needed to flag these gains against your historical residency and income records.

Practical FX Tips

USD in US → USD account in Japan

May help defer FX realization until conversion into JPY.Convert USD to JPY in US before remittance

Provides clearer visibility on the FX rate and transfer amount.Use FX tools strategically

Services such as Wise allow exchange rate alerts and timing flexibility.

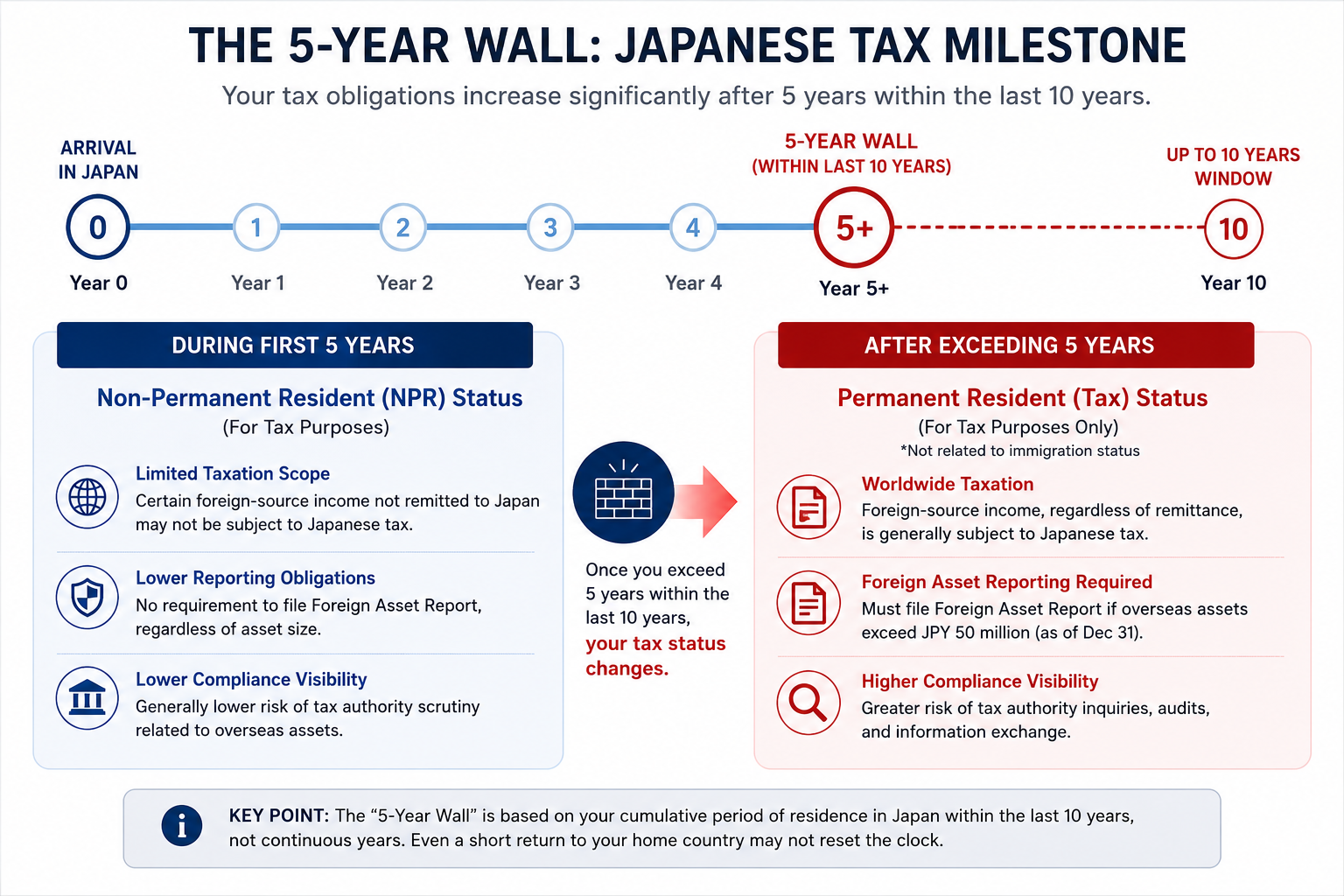

4. The 5-Year Threshold: NPR Status and Foreign Asset Reporting

For many international residents, the “5 years within the last 10 years” threshold is a major turning point in Japanese tax compliance.

Once this threshold is crossed, both reporting obligations and global tax exposure can increase materially.

The JPY 50 Million Rule

If your overseas assets exceed JPY 50 million as of December 31, you are required to file a Foreign Asset Report (国外財産調書) with the Japanese tax authorities by the following June.

This reporting obligation applies to both Japanese nationals and foreign residents who meet the applicable criteria.

Reportable assets may include:

overseas real estate

bank accounts

securities

insurance assets

private loans

cryptocurrency

The End of Non-Permanent Resident (NPR) Status

During the first 5 years, many foreign residents qualify as Non-Permanent Residents (NPR), which can limit Japanese taxation on certain foreign-source income not remitted into Japan.

After exceeding 5 years within the last 10 years, your Japanese tax classification generally shifts from Non-Permanent Resident (NPR) to “Permanent Resident for Tax Purposes” status.

⚠️This is a tax classification only and is unrelated to immigration Permanent Residency status

Important Practical Note

Joint overseas accounts can create reporting complexity. For example, US joint bank accounts are often reported using proportional ownership allocation (such as 50/50 between spouses). However, tax authorities also examine the actual source of funds behind the account.

Foreign Asset Reports may later affect international money transfers, inheritance reviews, gift tax analysis, and broader cross-border tax examinations.

See the Section 2/Essential Note: Residency for tax purposes

Property Titles in Japan: How Cross-Border Couples Can Avoid 2026 Tax & Inheritance Risks

Navigator Tip: US-Specific Complexity — 401k, IRA, and RMDs

For US Persons, moving retirement capital is a high-visibility event.

401k, IRA, and RMD distributions may be treated as taxable income in Japan once you become a Japanese tax resident, although treaty interpretation can become complex in practice.

More practical cross-border strategies and operational considerations will be covered separately in the free monthly Newsletter. Subscribe via the subscription button below.

5. Q&A

Q1: If I’m just moving my own savings, why does the National Tax Agency (NTA) care?

A1: The NTA's primary goal is to ensure the funds aren't "unreported gifts" or "unrecognized income". You must be ready to prove the capital was already taxed in its country of origin.

Q2:Are overseas accounts becoming more visible to tax authorities?

A2: Yes. Cross-border financial transparency has increased significantly in recent years.

Depending on your residency and citizenship status, overseas assets and accounts become subject to reporting regimes such as Japan’s Overseas Asset Reporting System (国外財産調書), international account information sharing frameworks (CRS), or US FBAR/FATCA rules.

6. Wrap-Up: From Risk to Resolution

International money transfer in 2026 is a formal declaration of your global financial status. The goal of this framework is not to hide wealth, but to ensure every JPY is "audit-proof" through meticulous documentation.

IMPORTANT COMPLIANCE DISCLAIMER

Transferring money between your own accounts is not itself taxable. However, depending on residency status and source of funds, the NTA may still treat certain transfers as taxable gifts, inheritance, or unreported income.

Consultation with a qualified cross-border tax professional is strongly recommended.

Related articles

Borderless Retirement: Strategic Positioning of U.S. Social Security in Japan (2026 Edition)

NISA and iDeCo for Foreign Residents in Japan: Practical Options for US Persons

Aki | Japanese | Former Head of HR in Global Finance

Aki has served as Head of Human Resources in the global financial sector.

With over two decades of experience navigating labor law, residency, and wealth protection in both Tokyo and Chicago, she now provides the "insider’s roadmap" for foreigners planning a stable, high-value long-term life and retirement in Japan.