How Much to Retire in Japan as an Expat: 2026 Costs, Visas, and Realistic Budgets

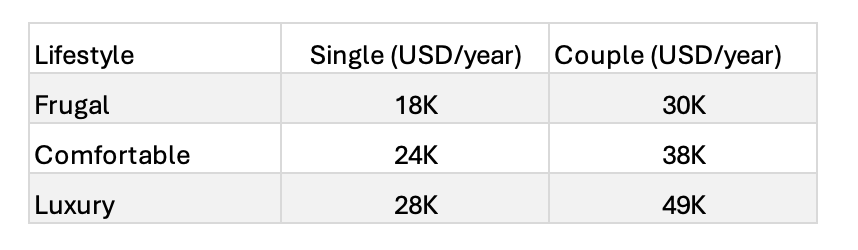

Quick Answer (2026 Estimate)

Single: USD 24,000/year

Couple (comfortable, outside Tokyo): USD 38,000/year

We moved to Japan — here’s what we actually feel after experiencing it firsthand.

(JPY159 = USD1 as of April 5, 2026)

Quick Summary

No dedicated retirement visa — what options work

Expat-specific extra costs: global tax filing, visa renewals, international travel, and currency risk

How much savings you need, including a buffer for longevity and unexpected events

Japan can be affordable vs. the U.S.

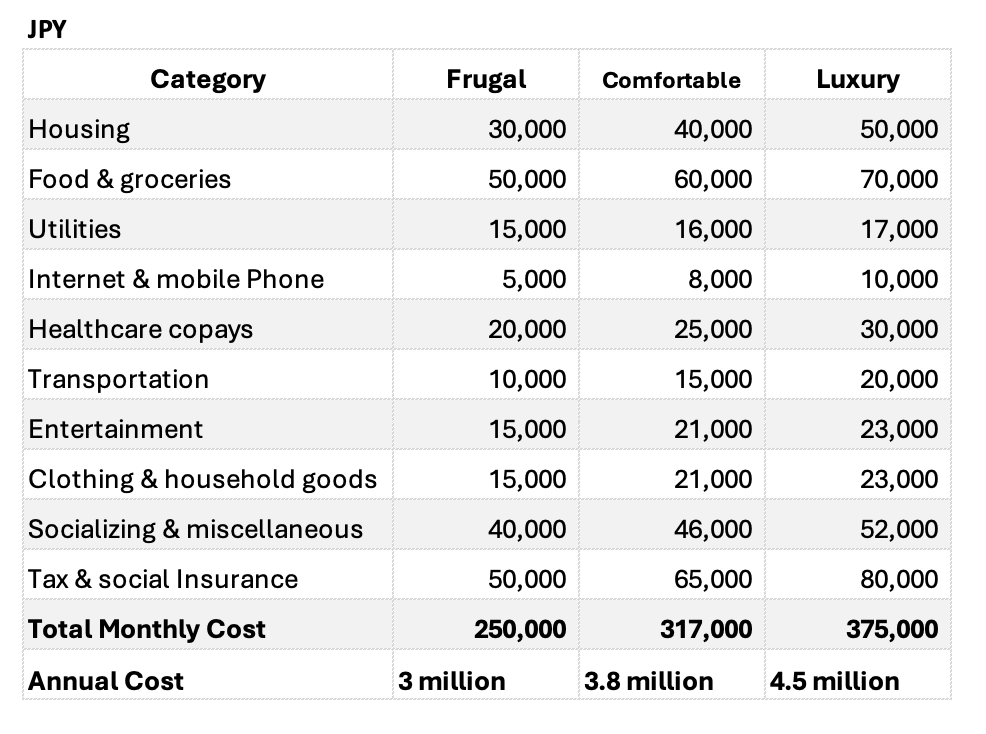

1. Monthly Cost for Singles (2026)

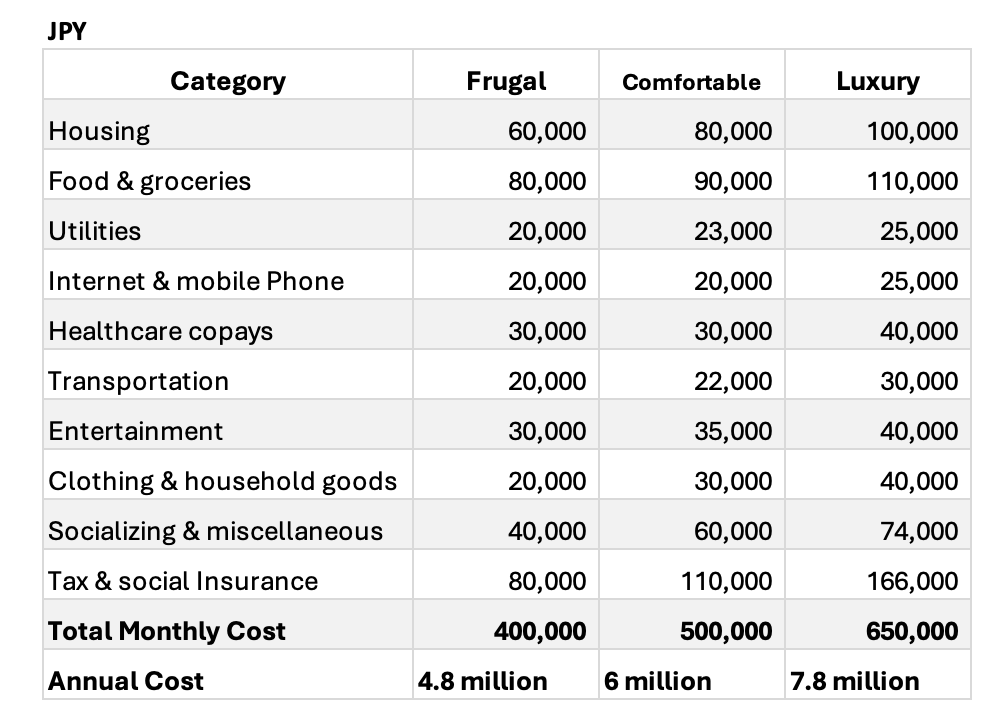

2. Monthly Costs for Couples (2026)

👉Notes for the Table:

These are planning-level averages for Tokyo. Actual monthly spending will vary depending on personal choices.

Housing costs assume the home is already owned outright, with no mortgage, and include property tax.

No child education expenses.

All figures include taxes, health insurance, long-term care insurance, utilities, and daily living expenses.

USD conversion rate: JPY159 = USD1 (as of April 5, 2026). Exchange rates fluctuate daily.

Three Lifestyle Tiers Explained

Frugal: Modest housing, cooking at home, limited travel.

Comfortable: Normal apartment, occasional eating out, some domestic travel.

Luxury: Premium housing, frequent dining out, regular international travel.

Your choice of tier and location has the biggest impact on how much money you need.

NavigatorJapan Tip

Foreigners typically incur additional costs for professional services such as global tax filing, inheritance planning, attorneys, and visa renewals. Most experienced providers are based in Tokyo, Osaka, and Fukuoka.

Go deeper: Where Should Foreigners Retire in Japan? A 4-Phase Framework for Choosing the Right Location

No Dedicated Retirement Visa — But Stable Options Do Exist

Japan does not have a specific retirement visa or passive-income pathway. However, many foreigners successfully build long-term lives here by securing other stable residence statuses well in advance.

Common pathways for those planning retirement include:

Permanent Residency (PR)

Spouse of Japanese National or Permanent Resident

Long-Term Resident status

Highly Skilled Professional route leading to PR

Immigration evaluates applications based on your overall financial self-sufficiency, savings, income, and compliance record.

Important note: Tourist visas cannot be used for retirement, and repeated short stays carry risk.

NavigatorJapan Tip

Starting visa planning while you are still working gives you the best chance of securing Permanent Residency or another stable status. This provides far greater peace of mind for your retirement years.

Additional Costs Foreign Retirees Often Face

Foreign retirees usually incur some extra costs that Japanese nationals typically do not. Being aware of these early allows you to plan proactively.

Key items include:

Currency Risk : The JPY can fluctuate 10–20% or more within a year. A stronger yen raises living costs for those receiving income in USD or EUR. Stress-test your budget using a conservative rate such as JPY130 per USD.

International Travel : Many expats return home periodically for family or administrative matters. Round-trip flights typically cost JPY250,000–JPY400,000 per person.

Global Tax Compliance : U.S. citizensand many others must file taxes in both Japan and their home country. After 5 years of residence, overseas asset reporting to Japanese tax authorities is also required. Budgeting for a specialized accountant is often necessary.

Visa and Residence Card Renewals : Most retirees rely on Permanent Residency or a spouse visa. Government fees are expected to increase significantly from 2027. Service provider and paperwork costs can add up.

Inheritance and Estate Planning : Japan has relatively high inheritance tax rates. Proper planning is important to avoid double taxation for heirs.

How Much Savings Do You Need?

To understand your real savings target, follow this practical 5-step framework:

Calculate your annual living costs minus reliable pension income or Social Security.

Multiply the shortfall by 25–30 to estimate the core savings needed.

Add a buffer of 3–8 years of annual living expenses for medical events, home repairs, currency fluctuations, and longevity risk.

Calculate your existing assets (savings, investments, real estate income, retirement accounts, etc.).

Compare the required amount with your current assets to see the actual gap.

This approach gives you a realistic picture of how much additional savings you may need to build before retirement.

Dual-pension couples are typically in a stronger position: They often benefit from two pensions, two retirement allowances, and combined savings.

Senior Care Costs: Japan’s mandatory long-term care insurance, substantial subsidies become available from age 65. However, assisted living or nursing home costs will still require additional out-of-pocket expenses.

NavigatorJapan Tip

Pensions provide stability. Savings provide flexibility and protection. Start with your desired lifestyle and location — these two decisions have the biggest impact on the final number.

Q&A

Q1. Can we live comfortably in Japan on U.S. Social Security alone?

A1. Sometimes— especially in regional cities. A couple receiving around $3,500 per month (Approx. JPY550,000) can live a Comfortable lifestyle in many areas, but currency risk should be carefully considered.

Q2. Do we pay tax on worldwide income?

A2. Yes. Once you become a Japanese tax resident, Japan taxes your worldwide income. Tax treaties help to avoid double taxation, but you must still report overseas assets and income. U.S. citizens also have ongoing FATCA and IRS reporting obligations.

Q3. Is private health insurance necessary?

A3. Usually no. Japan’s public health insurance covers most medical costs with low out-of-pocket maximums. For many people, it is often more reasonable to direct money toward savings rather than expensive private policies.

Q4. What happens if one spouse passes away?

A4. Survivor pension benefits may apply, but visa status and inheritance planning require early attention. Spouse visa holders typically need to change status within several months.

Q5. Can we keep a U.S. brokerage account after moving to Japan?

A5. It depends on the brokerage. Many U.S. firms restrict or close accounts for Japan residents. Check directly with your broker before relocating.