Will Your Accounts Freeze? Navigating Cognitive Decline & Banking in Japan [2026 Guide]

The Trillion "Ice Age"

A silent crisis is unfolding in Japanese bank vaults. By early 2026, an estimated JPY260 trillion ($1.7–$2 trillion) is held by individuals with cognitive decline.

In Japan, banks operate under a strict regulatory requirement to restrict account access once they identify a loss of mental capacity—a move intended to protect assets from fraud that often inadvertently locks out family members.

For those in their 50s or 60s, or anyone managing aging parents, understanding this regulatory landscape is a critical pillar of your residency strategy.

The Quick Navigator Summary

Risk: Accounts freeze if a clerk suspects cognitive decline—including Mild Cognitive Impairment (MCI)—or if a family member admits they are transacting for an incapacitated holder.

Bottleneck: Legal restoration of access typically takes 3–4 months, leaving you personally liable for mounting care costs.

Patch: Heirs can now withdraw up to 1.5 million yen for urgent needs, but this is a one-time, limited relief valve.

Solution: Proactive legal shielding via Voluntary Guardianship or Family Trusts is the only way to ensure 100% liquidity.

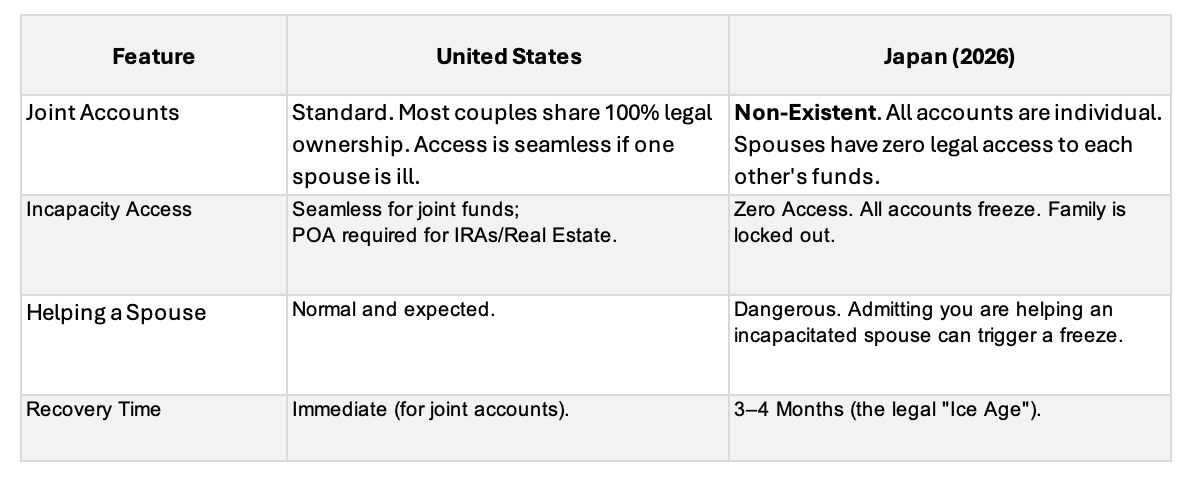

Cross-Border Risk Comparison: Why the U.S. Safety Net Fails in Japan

Table of Contents

Gateway Assessment

JPY1.5 Million Rule: A relief valve

Adult Guardianship - The Two Paths

Utilizing Trusts

Your 5-Step Anti-Freeze Checklist

Q&A

Wrap Up

1. Gateway Assessment

In Japan, bank clerks act as the front-line gatekeepers of cognitive health.

What the Clerk looks for during the interaction:

Repetition: Asking the same question three or more times in a single session.

Confusion over "Why": An inability to clearly state the purpose of a large withdrawal or transfer.

Document Management: Frequent reports of lost bankbooks or personal seals.

Unfounded Suspicions: Claiming bank staff have committed fraud or "stolen" money—a common symptom of advanced decline.

Other Check Points that trigger a freeze:

Erratic ATM Activity: Unusual or frequent high-volume cash withdrawals by the holder or family members.

Direct Disclosure: A family member inadvertently triggering a freeze by telling a clerk, "My spouse/parent is confused, so I am here to handle this for them."

Technical Triggers: Multiple incorrect PIN entries, attempts to cancel fixed-term deposits (teiki yokin), or complex investment transactions that require a level of verbal confirmation the holder cannot provide.

The Ripple Effect: It’s Not Just the Bank Account

Freeze extends far beyond your wallet. In Japan, if mental capacity cannot be verified, all legal contract-making may stop.

Real Estate Gridlock: You cannot enter into a sale agreement without the owner's verified intent. This means if you need to sell the family home to fund nursing home care, the property becomes effectively unsellable.

Contractual Paralysis: Because the holder can no longer legally sign contracts, everything from home repairs and renovations to signing up for new care services or managing investment portfolios comes to a complete halt.

The Navigator Tip: For international residents, a language barrier can often be misdiagnosed as cognitive decline.

If your spouse is the primary holder but has limited Japanese, they are at higher risk of an accidental freeze. This makes having Voluntary Guardianship and/or a Private Trust (discussed below) vital for residency security.

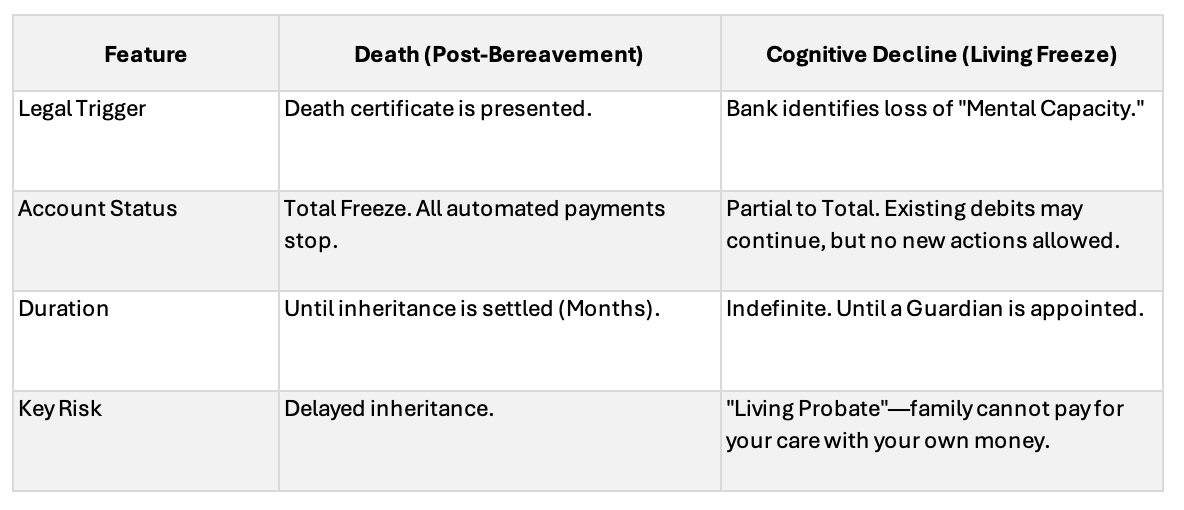

Sidebar: The Two Ways an Account Freezes

Many residents assume a bank freeze only happens at death. In Japan, cognitive decline triggers a freeze that can be even more difficult to manage.

2.JPY1.5 million Rule: A Relief Valve

Since 2019, Japanese law has allowed heirs to bypass a total account freeze for urgent financial needs.

The Rule: The heir can withdraw up to one-third of the account balance, capped at JPY1.5 million per bank, to cover immediate expenses such as funeral costs or hospital deposits.

The Reality for 2026:

Heavy Documentation: Access is not instant. Banks require extensive proof of inheritance rights, including Family Registers (Koseki Tohon) or Certificates of All Matters (Zenbu Jiko Shomeisho), and Seal Registration Certificates (Inkan Shomei). Gathering these can take weeks.

Institutional Variations: While available at most institutions (Banks, Shinkin, JA, Japan Post), procedures are not standardized. You must verify specific paperwork requirements with each branch in advance.

A One-Time Fix: This is a temporary measure, not a monthly allowance.

The Navigator Tip: Don't mistake this relief valve for a long-term plan. It is designed for emergencies, not for maintaining your family’s lifestyle or ongoing medical care during possibly a multi-year Bank Freeze.

3. Adult Guardianship (Koken-nin) - The Two Paths

If you need to manage savings, sell real estate, or sign contracts for care services, you must enter the Adult Guardianship System. While often viewed as a single process, it actually consists of two distinct paths: one proactive and one reactive.

A. Voluntary Guardianship (Nini Koken): The Proactive Choice

This is a contract established before cognitive decline occurs.

Control: You choose your guardian and define exactly what tasks they will handle on your behalf.

The Supervisor Fee: By law, the Family Court must appoint a supervisor to oversee the guardian. Even if you choose a family member as your guardian, the Supervisor’s fee is typically paid directly from your assets.

Limited Protection: Unlike the statutory version, a voluntary guardian does not have the legal right to cancel unauthorized contracts made by the account holder (e.g., a predatory purchase).

B. Statutory Guardianship (Hotei Koken): The Falling Back

While this can be used proactively, it is the only legal mechanism available once capacity is lost and an account is frozen.

Professional Reality: The Family Court selects the guardian. In over 80% of cases, they appoint a Japanese lawyer or scrivener rather than a family member.

Financial Burden: You must pay a monthly professional fee—typically JPY20,000 to JPY60,000 —from your savings for the duration of the guardianship.

Lifetime Commitment: Historically, once a guardianship begins, it cannot be terminated until the death of the holder.

The 2026 Reform Plan of Statutory Guardianship: A Move Toward Flexibility

The Japanese government has published a major overhaul to modernize the Statutory system, addressing its current rigidity:

Temporary Mandates: The system is shifting toward a model where guardianship can be terminated once a specific goal—such as the sale of a family home—is completed, rather than lasting for life.

Specific Support System: A new framework allows an appointee to focus on 11 key financial acts(including bank withdrawals and real estate transactions), granting them the power to cancel problematic contracts made by the holder.

Further details will become clearer as the legislative process progresses.

Internal Link: Japan Power of Attorney & Guardianship for Seniors: Overseas Families Need to Know Before a Crisis

Internal Link: Caring for Aging Parents in Japan from Overseas: What’s Realistic and How to Prepare

4.Utilizing Trusts

If you are currently in good health, establishing a Trust is one of the most effective ways to prevent a sudden bank freeze.

Unlike a Will (which triggers after death) or Statutory Guardianship (which often triggers only after a crisis), a Trust allows you to transfer asset management rights to a third party while you are still healthy.

Commercial Trusts vs. Family Trusts

There are two primary paths in Japan, each with distinct trade-offs:

A.Commercial Trust provides the peace of mind of bank oversight but is less flexible.

B.Family Trust offers maximum control but requires a high level of trust in the family member acting as your Trustee.

Always consult with a Judicial Scrivener (Shiho-Shoshi) or a specialist lawyer to determine which structure aligns with your specific family dynamic.

Hybrid Approach: A Robust Residency Strategy

For many international professionals, the goal isn't just protecting money, but ensuring total continuity of care. This often leads to a Hybrid Approach:

A.Trust (Asset Management): Whether Family or Commercial, the Trust acts as the financial engine, ensuring that funds for care, taxes, and maintenance remain accessible even if your personal mental capacity is questioned.

B.Voluntary Guardianship (Personal Care): This covers rights of personhood. It gives your chosen representative the legal standing to sign nursing home contracts, handle hospital admissions, and make medical decisions—critical tasks that a Trust (which only manages property) cannot perform.

Final Layer: Combining this hybrid approach with a Notarized Will ensures your inheritance strategy is equally seamless.

5.Your 5-Step Anti-Freeze Checklist

Don't wait for the first sign of memory loss. If you are over 60, complete these five steps to secure your assets.

[ ] Consolidate: Close zombie accounts. Centralizing assets reduces the number of gatekeepers you must navigate during a crisis.

[ ] Register a Proxy (Dairinin): Set up a bank-registered agent while healthy. It’s the fastest, lowest-cost way to maintain basic ATM access.

[ ] Automate: Move all utilities and taxes to Automatic Direct Debit. This ensures essential services continue even if manual withdrawals are restricted.

[ ] Formalize Legal Authority: Evaluate a Family vs. Commercial Trust for asset management and set up Voluntary Guardianship contractual and residential decisions.

[ ] Secure a Cash Bridge: Maintain three months of expenses in a separate account under a spouse’s or heir’s name to cover immediate needs during a legal transition.

6.Q&A

Q1: Can I use a foreign Power of Attorney (POA) to unlock a Japanese bank account?

A1: Generally, no. Japanese banks are notoriously rigid and rarely recognize private POAs drafted abroad, even with an apostille.

Once capacity is lost, the bank's only solution is a Court-Appointed Guardian. This is a reactive, crisis-only process that is slow, expensive, and often results in a court-appointed professional—not a family member—controlling the funds.

Q2: Will the bank freeze the account if I mention my spouse is getting forgetful?

A2: Yes; this is a significant risk. Once a clerk is on notice that a holder may lack capacity, compliance rules often trigger an immediate account restriction to prevent potential fraud or elder abuse.

To avoid this, it is safer to utilize a pre-registered proxy for transactions rather than disclosing cognitive struggles at the teller window without a legal plan already in place.

7. Wrap Up: The Cost of Waiting

In my years of experience, I’ve seen that the biggest hurdle isn’t the law or the cost; it is the human tendency to wait.

Seniors often hesitate to relinquish control, and family members—including myself—find it uncomfortable to bring up the topic of cognitive decline.

Please share your thoughts or questions in the comments below. Your experience could provide the vital insight another member of our community needs to hear today.

Official References (Japan)

Asahi: Frozen Bank Account Risks

Japanese Bankers Association: Account Handling After Death

MHLW: Adult Guardianship Portal

Aki | Japanese | Former Head of HR in Global Finance

Aki has served as Head of Human Resources in the global financial sector. With over two decades of experience navigating labor law, residency, and wealth protection in both Tokyo and Chicago, she now provides the "insider’s roadmap" for foreigners planning a stable, high-value long-term life and retirement in Japan.