Japan Health Insurance After Resignation 2026: Voluntary Continuation vs National – Which One Saves You Money Long-Term?

When you resign from a job in Japan — whether due to a career move, contract end, or a planned transition into retirement — one of the first practical decisions is how to manage your health insurance.

For foreign professionals on work visas or long-term residency, this is not only about monthly premiums. Health insurance is closely connected to pension contributions, visa status, and access to future healthcare systems.

As a result, even short gaps in coverage can have broader implications, such as interruptions in pension accrual or immigration.

The good news is that most of these issues can be avoided with early planning and a clear understanding of your options.

What This Article Covers

Quick Overview – Health Insurance

Why Health Insurance Continuity Matters in 2026–2027

When Seamless Transition Isn’t Possible: Your Two Options

2026 Cost Comparison

2026 Key Updates You Should Know

Q&A

Wrap-Up

1.Quick Overview – Health Insurance

If you stay in Japan for more than 3 months, enrollment in public health insurance is mandatory. This applies to all foreign residents, regardless of nationality or visa type.

National Health Insurance is for those outside standard employment—such as the self-employed, retirees, or the unemployed. It is managed by municipalities and is paired with the National Pension system.

Employee Health Insurance applies to those in qualifying employment. It is managed by employers or insurance associations, paired with Welfare Pension, and costs are split between employer and employee and deducted from payroll.

The key point:

When you leave a job, you are not simply switching insurance—you are shifting how you are covered across Japan’s healthcare and pension systems. This affects your costs, coverage stability, and ultimately your retirement outlook.

2.Why Health Insurance Continuity Matters in 2026–2027

Many foreigners underestimate how gaps in coverage affect their overall status in Japan.

Visa Risk Is Increasing

From June 2027, immigration enforcement is expected to tighten significantly. Authorities will cross-check health Insurance, pension and taxes.

These are increasingly reviewed together, not separately.

In practice, even short gaps or late payments can lead to delays in visa renewal, additional scrutiny, or in some cases, denial

This shift is already visible in permanent residency screening. Since the February 2026 revision, even a one-day delay in payments can significantly increase the risk of rejection.

Pension Continuity Is Indirectly Affected

Health insurance and pension are structurally linked. In Japan, anyone aged 20–60 with a registered address is required to participate in the public pension system.

In practice, gaps in health insurance often coincide with gaps in pension contributions. Continuous contributions are required, and any interruption directly affects both your eligibility and future benefits, potentially reducing your retirement income.

For foreigners, this is especially important. You generally need at least 10 years of contributions to qualify for a Japanese pension. If you leave before that, you may not qualify.

There are limited options to address this. A lump-sum withdrawal allows partial recovery of contributions, but your pension record in Japan is reset once you take it.

Alternatively, social security agreements may allow you to combine periods of coverage, depending on your home country.

Related article

Leaving Japan Vol.1: Visa, Exit Taxes, Pension Refunds, and What to Do Before You Go

Leaving Japan Vol.2: Practical Steps for a Smooth Departure

Future Healthcare and Senior Care Access

Health insurance continuity also affects your access to Japan’s long-term care system (介護保険).

From age 40, long-term care insurance becomes part of your coverage through the health insurance system. From age 65, you become eligible to use these services (or earlier in cases of certain certified conditions). Like health insurance, participation and payment are mandatory as long as you have residency in Japan.

In practice, breaks in coverage can lead to delayed or restricted access to services, higher out-of-pocket costs at the time of use, and fragmented records across municipalities.

Another important point is that the payment structure changes over time. Between ages 40–64, long-term care premiums are bundled with health insurance. From age 65, they are separated and typically deducted from your pension or paid via direct billing. This transition makes continuity even more important.

Real story

From my HR experience supporting foreign professionals in Japan, I’ve seen how easily these gaps occur. A friend left his corporate job to import Australian beef and start his own business. While employed, both health insurance and pension premiums were deducted automatically. He enrolled in National Health Insurance but forgot to apply for the National Pension, creating a two-month gap in his record. He caught it in time to make a back payment, but it could easily have reduced his future pension and complicated his visa renewal down the line.

The Ideal Scenario: Seamless Job-to-Job Transition

The lowest-risk path is a direct move from one employer to another with no gap in between.

In this case, your current coverage continues through your final day, and your new employer enrolls you from day one. This approach keeps costs shared between employer and employee, maintains pension continuity, and helps protect your visa status.

Where possible, securing your next role before leaving your current position helps ensure a smooth transition.

For those on National Health Insurance:

Skipping payments is the highest-risk scenario. If you are unable to pay, contact your local municipality early—there are often adjustment or installment options, but they require proactive communication.

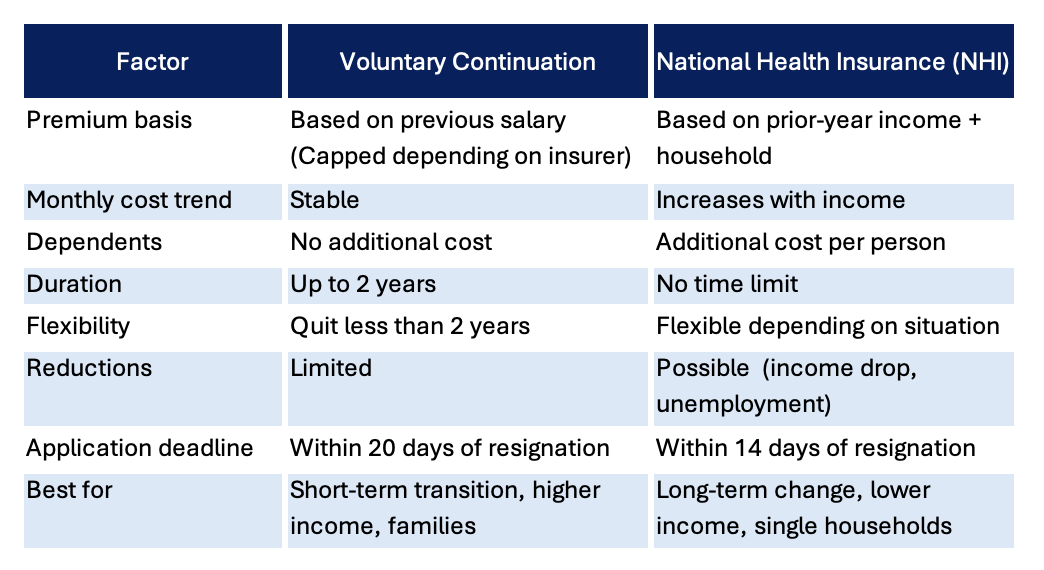

3. When Seamless Transition Isn’t Possible: Your Two Options

If you cannot transition seamlessly—due to a career break, starting a business, or unexpected job loss—you must choose between:

Employee Health Insurance Voluntary Continuation or National Health Insurance

The table below compares the two options across the key factors that matter most for long-term planning.

Once you understand how the two systems differ, the next step is to look at the actual cost impact.

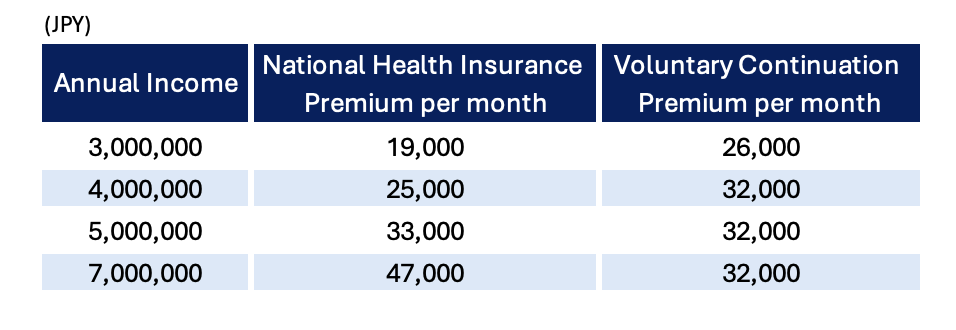

4.2026 Cost Comparison

To compare your options, start with your monthly health insurance premium from your payslip and double it, as the employer contribution will no longer apply.

Tip: Your final payslip often arrives after you’ve left (while using remaining paid leave) and may include two months of social insurance deductions. This can make the amount look unusually high—so don’t be surprised.

For National Health Insurance, use your municipality’s online calculator or confirm with your local office.

The example below reflects a typical profile of a single individual under age 40 (with long-term care insurance not included), living in Setagaya Ward, Tokyo.

Cost Comparison (Illustrative Example)

Key Points

Under voluntary continuation, premiums are typically capped under Kyokai Kenpo, keeping costs stable (around JPY32,000/month as of March 2026 in this example). A small discount may apply for 6–12 month advance payment.

In contrast, National Health Insurance is structured at the household level. Premiums are calculated based on income and household composition, meaning costs increase as additional family members are included.

In terms of coverage, the core medical benefits and co-payment rates are broadly the same. The main differences lie in how premiums are paid, whether dependents can be included, and the availability of additional benefits such as sickness allowance and maternity allowance, which are generally provided under employee-based insurance.

Decision Checklist (Use Before You Choose)

Do I have dependents? → Check premium impact with your local office

What was my last annual income? → Confirm using yourGensen Choshu Hyo.

Exit type (voluntary/involuntary)→ affects NHI discount eligibility

Am I planning retirement or self-employment? -> determines whether you need a long-term, flexible option (NHI)

Visa status → requires continuous, compliant payment records

5.2026 Key Updates You Should Know

Several updates in 2026 affect how both health insurance systems operate.

One notable change is the introduction of the Child and Child-Rearing Support contribution (0.23%),which began in April 2026.

This applies broadly to insured individuals, regardless of whether they have children. The contribution is scheduled to increase gradually through fiscal year 2028.

This measure uses the existing health insurance framework as a collection mechanism to support broader child and family policies.

Another important shift is the increased integration with the My Number system, including the move toward linking residence cards with My Number cards (effective June 14, 2026). This makes it easier for authorities to track records across health insurance, pension, and taxes—and, as a result, compliance is becoming more visible and more strictly enforced.

See the image below for the new My Number-linked residence card format effective June 2026.

6. Q&A

Q1: What happens if I miss the application deadline for voluntary continuation?

A1: You may lose the option entirely. In that case, you will typically need to enroll in National Health Insurance (NHI), which may result in higher costs or additional administrative steps. Note that NHI also requires you to apply within 14 days of leaving your job.

Q2: Can I switch between voluntary continuation and NHI later?

A2: It is now possible to voluntarily terminate continuation coverage. This means you can switch to National Health Insurance (NHI) when it becomes more cost-effective.

Q3: I am leaving Japan soon. Do I still need to enroll?

A3: Yes. Continuous coverage is required until your departure. Gaps can create complications in visa procedures, tax settlement, and pension records.

Q4: How do dependents affect the decision?

A4: Under voluntary continuation, dependents are covered at no additional cost. Under NHI, premiums increase for each household member, which can significantly raise total costs. Check with your local city office for the exact impact.

Q5: I am unemployed. Which option is usually better?

A5: If your income drops, National Health Insurance (NHI) may offer reduced premiums depending on your situation. Voluntary continuation, on the other hand, is based on your previous salary and does not adjust downward.

Q6: What if my income was high before leaving my job?

A6: Voluntary continuation is often more cost-efficient for higher incomes because premiums are capped (especially under Kyokai Kenpo), while NHI increases with income.

Q7: Do I need to pay both health insurance and pension after leaving my job?

A7: Yes. These are separate obligations. You will need to arrange both health insurance and pension payments unless you qualify for specific exemptions.

Q8: What if I cannot afford National Health Insurance or pension payments temporarily?

A8: Do not skip payments. Contact your municipality as early as possible—there may be installment plans or reductions available depending on your situation.

7. Wrap-Up

Next in the Japan Practical Stability 2026 Series

Now that you’ve seen how today’s health-insurance choice directly affects your pension accrual, visa records, and future senior-care access, the next step is locking in the long-term residency status that makes those contributions count.

Next, we’ll cover Permanent Resident, Long-Term Resident, and Spouse visas in 2026–2027 — the new 5-year rule, how payment records are cross-checked, and which path best protects your retirement stability. This series connects every practical decision (insurance, visas, pension, job changes, health risks) so you can build real long-term security step by step.

If you have experiences, tips, or questions, please share them in the comments.

And if you found this article helpful, please consider sharing it with friends, family, or colleagues who are living in or planning to move to Japan!

References

Why Immigration Is Becoming Stricter in Japan (2026–2027 Trend)

What Japan Looks at for Permanent Residency Approval

Official PR Application Rules (Japan Immigration)

See also

The Real Fork for Foreign Professionals in Japan: Why Your 40s Decisions Lock In Your Life After 60

How Much to Retire in Japan as an Expat: 2026 Costs, Visas, and Realistic Budgets