The Real Fork for Foreign Professionals in Japan: Why Your 40s Decisions Lock In Your Life After 60

Most people think retirement is decided at 60. In reality, it is largely determined much earlier—during your 40s. The critical window is mid-40s to early 50s—when options are still open and outcomes are set.

I learned this the hard way. I waited until after retirement to launch NavigatorJapan—too busy, or so I told myself, to prepare seriously for what comes next. In hindsight, that was simply an excuse.

The encouraging reality is that even those who continue working until 65 still have 10 or more meaningful years to build a second chapter. But those who thrive are usually the ones who began building independent options earlier—while mobility still existed.

This is the logic behind the 4-phase framework for long-term life in Japan.

What Are the 4 Phases of Retirement in Japan?

1. Mobility

Late-career decisions that preserve flexibility before labor mobility narrows

2. Stability

The early retirement years when individuals must build a personal system for income, healthcare, taxation, and administrative obligations.

3. Dependency

Later-life planning for healthcare coordination, legal authority, and financial liquidity during potential health decline.

4. Legacy

Cross-border inheritance planning to ensure assets, documentation, and legal structures can be executed smoothly across jurisdictions.

Related article: The 4 Phases of Retirement in Japan: A Framework for Foreign Residents Planning Long-Term Life

This article covers:

1. Why Mobility Matters More Than Most Realize

2. Realistic Paths After 60 — All Valid, But Preparation Changes Everything

3. What Works: 40s Moves That Unlock Life After 60

4. Mobility-Phase Checklist: 5 Moves to Start Today

5. Wrap Up

1.Why Mobility Matters More Than Most Realize

The mobility phase in 40’s is busy. Promotion races are still active, responsibilities are heavy, and leadership roles may finally be within reach. At the same time, life outside work becomes more demanding — mortgages, children’s education, and sometimes the early stages of caring for aging parents.

Yet this is also when the fork in the road quietly appears.

Every decision in the Mobility phase affects multiple systems at once — including work, pension, healthcare, and visa/residency status.

Related article:

How Much to Retire in Japan as an Expat: 2026 Costs, Visas, and Realistic Budgets

The Retirement Checklist for Japan (2026 Edition)

2. Realistic Paths After 60 — All Valid, But Preparation Changes Everything

With life expectancy extending retirement into 20–30+ years, most foreign professionals in Japan follow one of three paths. Preparation during the Mobility phase determines how sustainable each becomes.

Path A — Continue Working

Many extend their careers into their late 60s or 70s for income, engagement, and identity. This typically takes the form of re-employment or fixed-term contracts with the same employer, as external hiring becomes more limited after the mid-50s.

In the short term, this path offers relative stability, including continued visa sponsorship. However, without skills or networks built in the 40s, it creates a growing dependency on a single employer—exposing individuals to narrowing re-employment options, pension gaps after 65, and increasing visa pressure if sponsorship ends.

Path B — Full Freedom

Others step away completely to prioritise travel, family, hobbies, or relocation. While rewarding, this path removes employer sponsorship entirely and places full responsibility for income, pension, healthcare, and residency on the individual.

In practice, this path is only viable with the right visa status. Without Permanent Residency (PR) or a spouse visa, staying in Japan without employment is extremely difficult. This turns what appears to be a lifestyle choice into a structural constraint that must be solved upfront.

Without early planning, this becomes a high-stakes convergence: pension timing decisions, National Health Insurance transitions, and visa/residency continuity must all be managed simultaneously.

Path C - The Hybrid Path (Work and Freedom)

Increasingly popular among experienced foreigners, this path blends purposeful activity with flexibility—work closer to ikigai (生きがい) than traditional employment.

When built from the 40s, it creates strong horizontal protection: a side-income stream that supports National Pension contributions (generally based on 20+ hours/week), while preserving healthcare access and workload flexibility.

Like Path B, it depends on having the right visa foundation. Without Permanent Residency (PR) or a spouse visa, flexible or part-time work is highly restricted. Alternatives—such as a Business Manager visa—require strict business continuity and are difficult to sustain at a small scale.

Without independent, marketable skills or a strong network, options are often limited to physically demanding or lower-paid roles.

All three paths are valid. None, however, is automatic.

Re-employment until 65 only covers the opening chapter. The quality of the next 15–25 years is written in the Mobility phase.

Related article: Navigating Mandatory Retirement in Japan and Life After 60

3. What Works: 40s Moves That Unlock Life After 60

Foreign professionals who experience the most flexibility and lowest stress after 60 are almost always those who made one deliberate move in their 40s to reduce dependency on a single employer or visa sponsor.

These are not success stories. They are early decisions that created optionality.

The patterns are consistent:

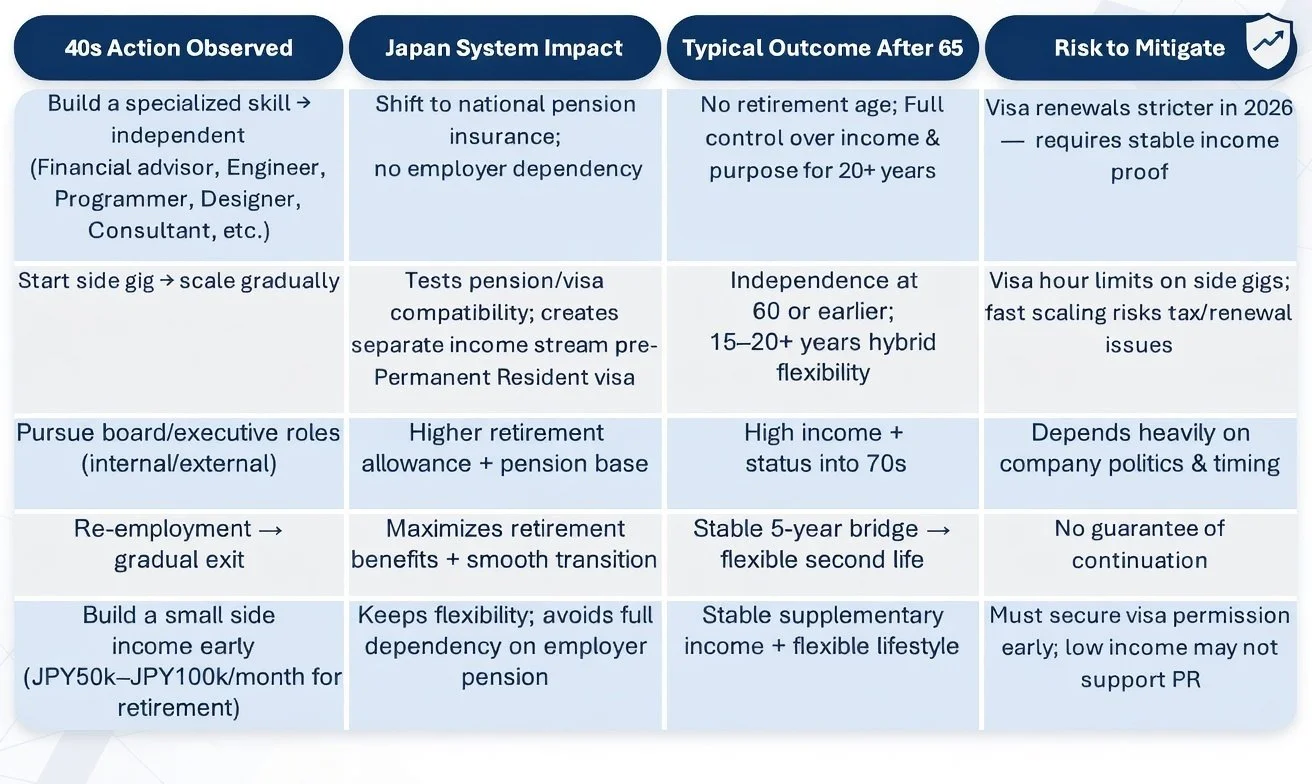

Each row reflects a different strategy—but the underlying logic is the same: reduce dependency early, and options expand later.

Case 1: Build a specialized skill → independent

He was an IT head from India, covering everything from operations to risk and compliance. When he heard about mandatory retirement, he refreshed his programming skills. By his early 50s, he transitioned into independent consulting with multiple project-based contracts in the financial sector.

Now in his early 60s, he works entirely on his own terms—flexible, self-directed, and independent of corporate timelines.

Note: He remained under an Engineer/Specialist in Humanities/International Services visa while operating as a sole proprietor. Maintaining multiple client contracts is critical to demonstrate income continuity (see table row 1).

Case 2: Start side gig → scale gradually

During the pandemic, she started a YouTube channel focused on business skills and logical thinking. Over time, she grew it to over 100,000 subscribers while remaining fully employed. Before retirement, she transitioned into independent business coaching.

Note: Side work is increasingly accepted, but company approval is often required to avoid conflicts of interest. Early validation of income streams reduces both financial and visa risk (see table row 2).

Related article

Can Foreign Workers Do Side Jobs in Japan? Visa Rules, Risks, and Why You Need a Backup Plan

Case 3: Pursue board/executive roles (internal/external)

Foreign representation on boards in Japan remains limited and often tied to expatriate assignments. As a locally hired financial professional from Australia, he recognized this constraint early.

Instead of relying on internal promotion, he built a strong local network and positioned himself strategically. This led to a COO role at a new financial firm, and eventually a board position. He now serves as an independent director.

Note: Network leverage—especially combined with international exposure and Japanese proficiency—can unlock non-traditional paths, including regional opportunities (see table row 3).

Case 4: Re-employment → gradual exit

As mandatory retirement approached, he faced two options: early retirement with severance or re-employment under reduced terms. As he was applying for Permanent Residency (PR) after 10 years in Japan, he chose to remain employed to support his application, despite the reduction in compensation.

In Japan, this typically takes two forms: re-employment (retire with a retirement allowance and rehire under new terms) or extended employment (continuation of the existing contract). The former allows significant changes in compensation and role, while the latter tends to preserve more stable conditions.

Note: Re-employment often provides a structured 3–5 year bridge, but continuation is not guaranteed. Once PR is obtained, visa constraints are removed, allowing transition to Path B or C without restriction after employment ends (see table row 4).

Case 5: Build a small side income early (JPY50k–JPY100k/month after retirement)

She was an HR professional from New York who developed woodworking as a hobby. While still employed, she invested time in building her skills and began selling her work.

The income remained modest, but after retirement, it became a steady and flexible source of supplemental income.

Note: She held a spouse visa, allowing flexibility. This began as exploration—identifying skills that could generate income. Starting in her 40s made the transition natural and sustainable (see table row 5).

These paths all require early action during the Mobility phase.

In reality, this is often when you are busiest—making it easy to delay long-term thinking. Yet this is exactly the invisible fork where small, deliberate actions create lasting differences.

4.Mobility-Phase Checklist: 5 Moves to Start Today

The early Mobility phase is when leverage is highest and structural dependencies are easiest to reduce. Each action below is designed to protect at least two critical domains simultaneously: visa continuity, pension accrual, tax residency, and cross-border flexibility.

This is not about making drastic changes. It is about building optionality while it is still possible.

The checklist below is not about optimization — it is about avoiding constraints that become difficult, or impossible, to reverse later.

A.Direction: Clarify Your “Stability Phase” Vision

Clarify — at least roughly — the shape of life after 60:

Full-time or contract work / complete freedom / hybrid activity?

Remain in Japan full-time / dual-country base / eventual relocation?

Primary driver: income security / purpose / lifestyle flexibility?

A clear (even provisional) direction sharpens every downstream choice: job moves, savings allocation, visa strategy, and family discussions. Without it, decisions default to inertia.

B. Capability: Build Portable, Aging-Well Skill + External Network

Prioritise capabilities that retain value beyond traditional employment:

Deep specialised expertise (technical, regulatory, advisory)

Teaching, consulting, or cross-border services

Product or business-building thinking

Japanese language proficiency

General corporate management skills alone rarely generate post-60 income.

At the same time, intentionally build a professional network outside your current employer — most viable opportunities after mandatory retirement emerge through relationships, referrals, and reputation, not open job postings.

Goal: Validate at small scale while still employed. Even modest, recurring income (e.g., JPY 50,000–100,000/month) creates a foundation for hybrid or independent paths.

Note: annual side income > JPY 200,000 usually triggers a tax filing obligation.

C. Legal Flexibility: Enable Side Activity Early

If you are on a work visa, confirm what is permitted beyond your primary employment and enable limited activity early.

Side gig typically requires “Permission to Engage in Activities Other Than Those Permitted”

Start small—testing compatibility matters more than income size

Even modest side income may trigger tax filing obligations

This step is about activation: proving that additional income streams are legally and operationally viable before you depend on them.

D. Independence: Secure Status & Reduce Structural Dependency

Identify where you are structurally constrained and begin reducing those dependencies:

Employer-sponsored visa

Company-linked housing or benefits

Geographic immobility

The priority is to secure status, not just flexibility.

Build momentum toward Permanent Residency (PR)

Maintain clean tax, pension, and residency records

Anticipate tightening policy trends (e.g., higher application/renewal fees and stricter review)

Without independent status (PR or equivalent), many post-60 options—especially Path B and C—remain structurally limited.

E. Integration: Align Cross-Border Financial & Family Structures

Do not delay alignment across countries and systems:

Inventory assets, pensions, and accounts across jurisdictions

Update beneficiaries across all financial instruments

Discuss care expectations, location preferences, and family roles

Prepare a basic “emergency file” (wills, powers of attorney, contacts)

These 5 moves are cumulative — each reinforces the others.

Implemented gradually in your 40s, they create horizontal protection across Japan’s institutional systems—something most professionals address in isolation through separate experts (HR, tax, immigration).

5. Wrap Up

The real fork is not retirement at 60.

It is the set of decisions you make in your 40s—often without realizing their long-term consequences.

What looks like a choice later is often the result of preparation made much earlier. The difference between constraint and flexibility after 60 is rarely accidental.

The encouraging reality is this: when you use the Mobility phase well, the years after 60 can be flexible, self-directed, and meaningful—whether through work, contribution, or personal pursuits.