Japan Pension Guide 2026 [Maximize Payouts + New Rules]

Will you actually receive a meaningful Japan pension after years of contributions—or risk losing your eligibility when you leave?

For long-term residents, the true value of the system hinges on two factors: social security totalization and the looming expansion of withdrawal limits.

This guide provides the exact 2026 payout figures, a breakdown of the unexecuted 8-year rule, and the common compliance mistakes that can derail your Permanent Residency (PR) or retirement.

Table of Contents

Quick Summary – 2026 Essentials

The Compliance Gap: Your Visa & PR at Risk

2026 Payouts: The "JPY500k Gap"

The 8-Year Lump-Sum Update

Totalization: The 10-Year "Secret"

Practical 2026 Checklist

Q&A

Wrap Up

1.Quick Summary – 2026 Essentials

(Using the current April 9, 2026 rate of JPY158.69.)

The Navigator Strategy: If you plan to retire in Japan long-term, avoid the lump-sum withdrawal. The lifetime value of a monthly pension almost always exceeds a one-time payment.

2. The Compliance Gap: Your Visa & PR at Risk

In my experience as an HR professional, job transitions are the danger zone. If you resign or change jobs, you must manually switch to the National Pension within 14 days at your ward office.

Immigration Impact: For 2026 Permanent Residency (PR) applications or visa renewal, Immigration checks for even a single "missing month." A late payment isn't just a fee; it can lead to an immediate visa rejection.

Real Story: The Start-up Trap: An Australian client resigned to launch an import business. During the frantic start-up phase, he registered for Health Insurance but forgot the National Pension for two months. We caught it just in time—he retro-paid the premiums to clean his record before his PR filing. Don't let administrative "busy-ness" cost you your residency.

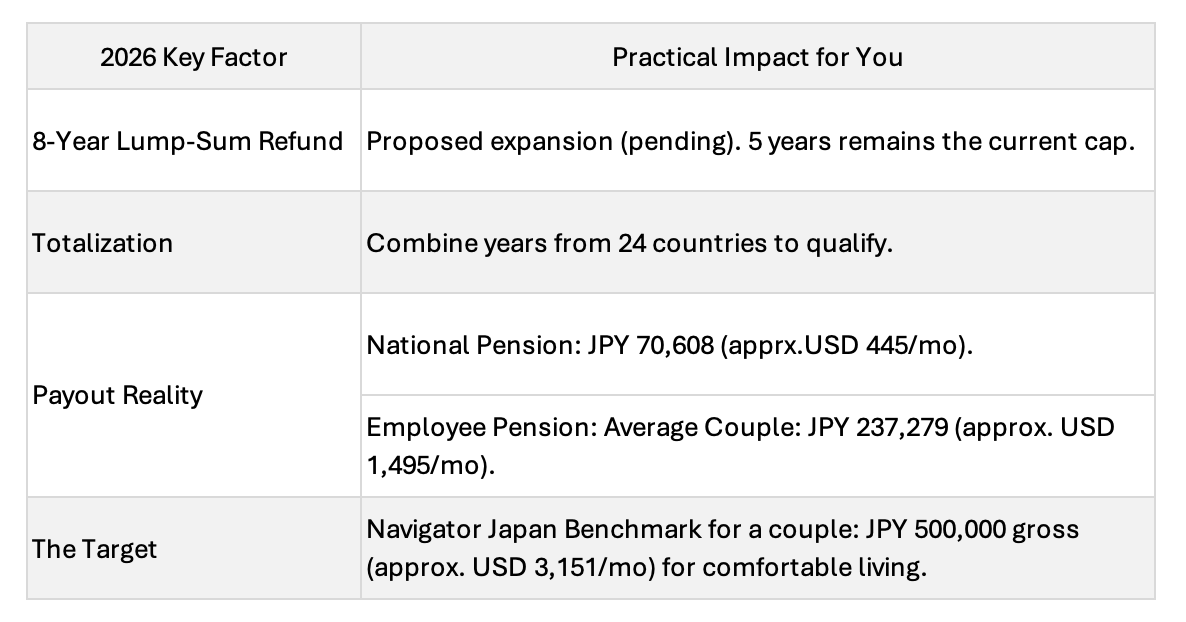

3. 2026 Payouts: The "JPY500k Gap"

The government adjusted 2026 payouts for inflation, but they still won't cover a Western-standard retirement alone.

National Pension (Full): JPY70,608 / month.

Employees' Pension (Average Couple): JPY237,279 / month.

Note on the "Average Couple" Figure: This JPY237,279 benchmark is the government’s "Model Household" estimate. It assumes a husband who earned an average monthly salary of JPY455,000 (including bonuses) for 40 years, and a dependent wife who receives the Full National Pension.

The Power of Deferral: Increasing Your Monthly Check

If you don't need the cash immediately at 65, you can choose to delay your pension start date up to age 75.

0.7% Rule: For every month you delay claiming your pension past age 65, your monthly benefit increases by 0.7% for life.

The Result: Delaying until age 75 results in an 84% permanent increase in your monthly payout. For many expats, working a few extra years to "lock in" this higher rate is the most effective way to close the retirement gap.

The Navigator Japan Benchmark: We estimate a couple’s comfortable expat retirement in non-central Tokyo requires JPY 500,000 gross/month. Subtract your pension from this target to find your "Gap"—this is what your NISA and iDeCo must cover.

Related article: How Much to Retire in Japan as an Expat: 2026 Costs, Visas, and Realistic Budgets

4. The 8-Year Lump-Sum Update

If you leave Japan permanently, you can claim a Lump-Sum Refund (Dattai Ichijikin).

The Expansion: The government is moving to expand the cap to 8 years. However, as of April 2026, the 5-year (60-month) cap remains the official legal limit.

The 2-Year Deadline: You must apply within 2 years of leaving Japan.

The 20.42% Tax Trap: Employees' Pension refunds are taxed at 20.42% at the source. To recover this, you must appoint a Tax Agent (Nozei Kanrinin) in Japan before you depart to file a tax return on your behalf.

5. Totalization: The 10-Year "Secret"

You can combine years worked in 24 countries (US, UK, Australia, etc.) to meet the 10-year vesting requirement.

The 10-Year Vesting Rule: Normally, you need 10 years of Japanese contributions to qualify for a pension.

The Shortcut: Under totalization, 7 years in the US and 3 years in Japan = 10 years. You will receive a pro-rated Japanese check for those 3 years at age 65.

Navigator Update: The WEP Repeal(2025/2026) For years, American expats faced the "Windfall Elimination Provision" (WEP), which slashed their US Social Security benefits if they also received a Japan pension. The Good News: As of January 2025, the WEP has been officially repealed. US expats now receive their full Social Security benefits alongside their Japan pension. If you are already retired, ensure you have received your retroactive adjustment payments from the SSA.

6. Practical 2026 Checklist

Don’t leave your retirement to chance. Complete these four critical audits to bridge the gap between your pension and your actual needs.

[ ] The "Nenkin Net" Forensic Check: Log in to catch employer reporting errors in real-time. Look specifically for "Blank Months" during job transitions. For expats, a single missing month isn't just a loss of money; it's a "Compliance Red Flag" that can derail a 2026 Permanent Residency (PR) application.

[ ] The Dual-Income "Gap" Forecast: When your Nenkin Teikibin (the birthday envelope) arrives, don't look at it in isolation.

The Navigator Japan Benchmark: We aim for JPY 500,000 gross/month for a comfortable couple’s lifestyle.

The Nuance: If you are a dual-income household, combine both your projected checks. If you each receive JPY 180,000, your household total is JPY 360,000—shrinking your "Gap" to a much more manageable JPY140,000.

[ ] The 401k/iDeCo "Bridge": Your pension is only Layer 1. Audit your Layer 2 assets (US 401ks, UK SIPPs, or Japan’s iDeCo).

Calculated Strategy: If your 401k can safely provide USD 1,000 (approx. JPY 158,000) per month, you have effectively closed a massive portion of the gap before touching your NISA savings.

[ ] Retroactive "Gap" Recovery: If you find missing months from the last two years, pay them immediately. The 2026 National Pension rate is JPY17,920/month. Think of this as a "Residency Insurance" payment—it keeps your record clean for Immigration while slightly boosting your lifetime payout.

7. Q&A

Q1: What if I move back to the US before I turn 65?

A1: You claim your pension from abroad. JPS wires JPY to your US bank. Your local US Social Security office can help with the paperwork.

Q2: Can my non-Japanese spouse receive my pension?

A2: Yes. If you have 20+ years in the Employees' Pension, a dependent spouse may qualify for a Survivor’s Pension.

Real Story: The Language Barrier A friend lost her husband and was overwhelmed. Japan Pension Service (JPS) documents are almost exclusively in Japanese. Navigating survivor benefits without professional help or high-level Japanese is nearly impossible during a time of grief. Identify a professional service or trusted bilingual support before a crisis hits.

Q3: Can I pay into the system past age 60?

A3: Yes. National Pension contributions are generally required from ages 20 to 60 (40 years for full coverage). However, if you are enrolled in Employees’ Pension (e.g., as a company employee or civil servant), contributions can continue up to age 70.

You may also voluntarily continue National Pension contributions until age 65. The longer you contribute, the higher your future benefits.

Note: You only need a minimum of 10 years of contributions to qualify for benefits.

8.Wrap-Up: The Navigator’s Final Tip

Japan Pension Service (JPS) offices currently have a 1-2 month waiting list. Walking in can take hours. Call today to book your consultation.

Bring to your appointment:

My Number Card / Zairyu Card

Pension Book (Nenkin Techo)

Bank details for deposits

Home country pension records

Share your specific situation in the comments below.

I read every entry and will provide guidance as much as possible.

Official 2026 Resources:

JPS: Early or Deferred Pension Benefits (Advance / Delayed Claiming)