The 4 Phases of Retirement in Japan: A Framework for Foreign Residents Planning Long-Term Life

A cross-border, executive-level framework

Retirement is often described as a financial milestone. In reality—especially for foreigners building a long-term life in Japan—it is a multi-stage institutional transition.

The 4-Phase model is not unique to Japan. It reflects how retirement transitions unfold globally. However, Japan’s institutional structure—mandatory retirement practices, pension replacement levels, and exceptional longevity—makes these phases particularly visible.

Most people prepare financially. Far fewer prepare structurally.

Executive Summary

What Are the 4 Phases of Retirement in Japan?

1. Mobility

Late-career decisions that preserve flexibility before labor mobility narrows (visa status, asset location, work options).

2. Stability

The early retirement years when individuals must build a personal system for income, healthcare, taxation, and administrative obligations.

3. Dependency

Later-life planning for healthcare coordination, legal authority, and financial liquidity during potential health decline.

4. Legacy

Cross-border inheritance planning to ensure assets, documentation, and legal structures can be executed smoothly across jurisdictions.

These phases reflect how retirement interacts with immigration status, pension systems, healthcare access, tax residency, and family governance.

For foreigners in Japan, retirement planning must integrate:

Immigration/Visa

Tax residency exposure

Healthcare and senior care system integration

Asset location and liquidity

Late-career employment constraints

Inheritance execution across jurisdictions

The earlier you recognize the phases, the more control you retain.

In this article, we cover:

Why a 4-Phase model

Phase 1 — Mobility

Phase 2 — Stability

Phase 3 — Dependency

Phase 4 — Legacy

What HR can say (and do) using this model

Wrap Up

1. Why a 4-Phase model

Mindset follows incentives. Systems create behavior.

OECD Employment Outlook data shows how different retirement behavior can be across countries.

In Japan, employment among older adults remains unusually high:

74.4% for ages 60–64

53.5% for ages 65–69

In the United States, employment declines much more quickly:

56.7% for ages 60–64

32.4% for ages 65–69

This gap is not just “work ethic.” It reflects institutional design: pension adequacy, labor market structure, health-cost exposure, and how identity is anchored (organization vs individual career capital).

For example, OECD pension modeling 2022 shows net replacement rates for an average earner of approximately:

Japan: 38.8%

United States: 50.5%

Lower pension replacement combined with one of the world’s highest life expectancies creates a rational incentive to continue working longer in Japan.

For foreign residents, these institutional differences help explain why retirement often unfolds in distinct phases rather than as a single financial decision.

2. Phase 1 – Mobility

Protecting Optionality Before It Shrinks

When: Late career through early transition (often 45–65)

Primary Risk: Loss of flexibility

In Japan, late-career labor mobility compresses sharply. Mandatory retirement structures, re-employment contracts at reduced salary, and corporate risk aversion narrow the window of professional leverage as employees approach retirement age.

For foreign residents, this phase includes additional cross-border structural risks that can significantly shape future options.

Cross-Border Specific Risks in Mobility

Immigration status

Late-career visa decisions can lock in—or restrict—future options. Securing Permanent Resident (PR) status before retirement removes sponsor dependency (employer or spouse), providing indefinite residence and eliminating renewal risks after leaving full-time employment.

Tax residency transition

Remaining in Japan long enough may trigger “permanent resident for tax purposes” status (generally after 5 years of residence within the past 10 years). Once this threshold is reached, global income reporting obligations expand significantly.

Asset location complexity

Many expats maintain retirement assets in their home country (for example, U.S. 401(k)s or IRAs) due to investment flexibility or tax treatment. However, these accounts create ongoing cross-border obligations involving reporting, required minimum distributions (RMDs), beneficiary access, and eventual estate administration.

Mobility Phase – Irreversible Decisions Checklist

If your income stopped in a given year, where would your liquidity come from?

How portable is your professional identity—could you continue working in another location or system?

Does your residency structure support where you plan to live in the future?

Have you stress-tested pension timing against realistic longevity scenarios?

Strategic Decisions in the Mobility Phase

NOTE: For US persons, see NISA and iDeCo for Foreign Residents in Japan: Practical Options for US Persons

Real Story

In Japan, many employees begin seriously planning for retirement in their 50s, when they realize they have likely reached their final position within the organization. Many companies also operate a system called yakushoku teinen (役職定年),where managers step down from leadership roles—often between ages 55 and 60—to allow generational turnover.

Related article: Navigating Mandatory Retirement in Japan and Life After 60

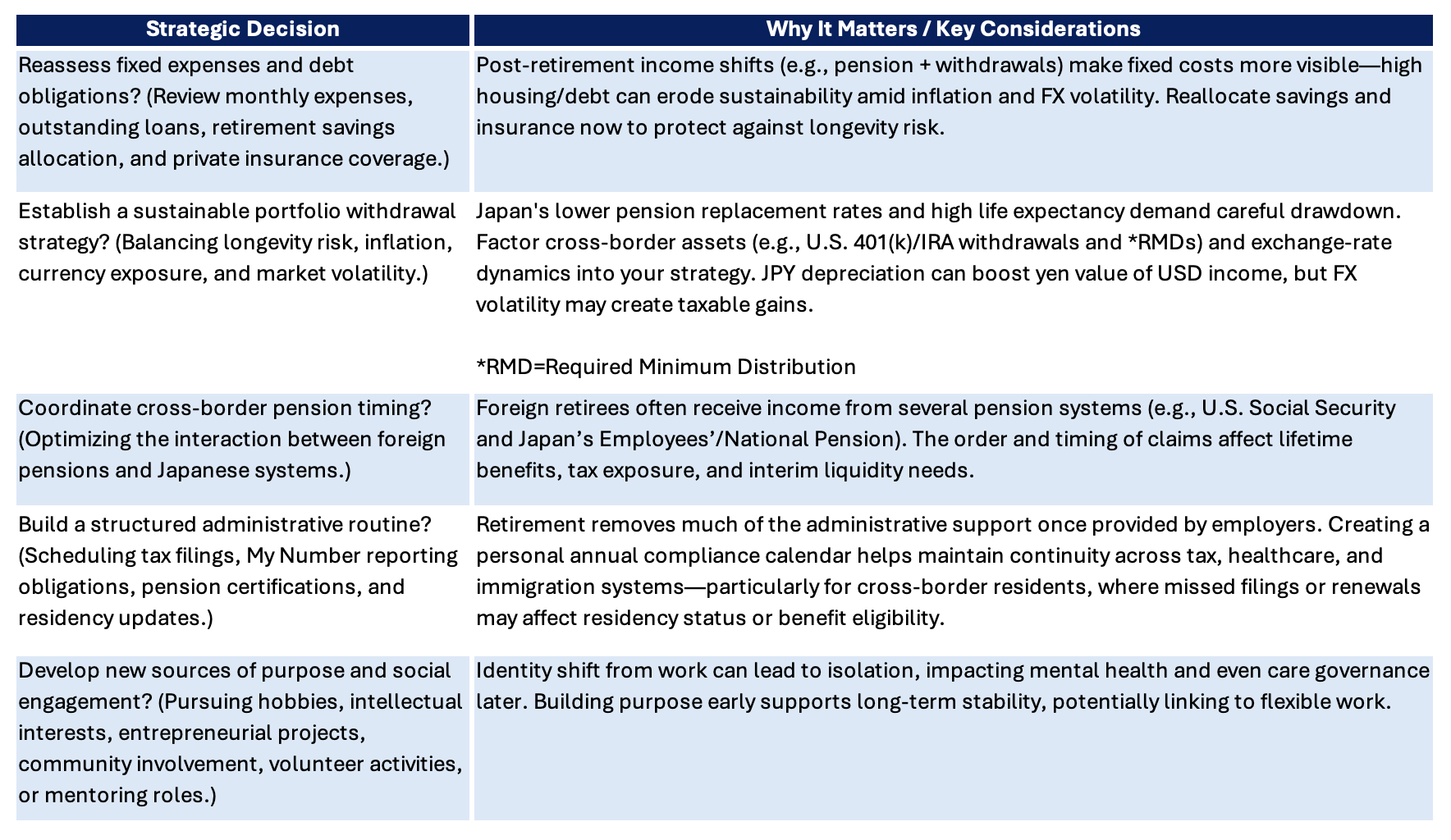

3. Phase 2 – Stability

Building a Personal Operating System

When: Retirement (often 55–75)

Primary Risk: Administrative and identity shock

Retirement is frequently described as freedom. But freedom removes structure.

During the Stability phase, the institutional framework that once organized daily life—salary, employer benefits, and corporate administration—largely disappears. Retirees must replace that structure with a personal operating system that coordinates healthcare, income management, taxation, and administrative obligations across jurisdictions.

Cross-Border Specific Risks in Stability

Healthcare system transitions

Upon retirement, individuals may either continue their employer health insurance (任意継続) for up to two years without employer contributions or transition to National Health Insurance. Premiums should be compared carefully to determine the more cost-effective option. As healthcare needs increase with age, securing access to a reliable primary physician becomes increasingly important.

Longevity mismatch

OECD data shows life expectancy of approximately 84 years in Japan vs. about 78 years in the United States, increasing the probability that retirement will last 30 years or more. A longer lifespan extends the period during which retirees must manage chronic health risks, inflation exposure, and portfolio sustainability.

Cross-border pension coordination

Many retirees must coordinate multiple pension systems—for example, U.S. Social Security benefits alongside Japan’s Employees' Pension Insurance (Welfare Pension) and/or National Pension (basic pension). Totalization agreements help avoid double contributions, but reporting requirements, taxation rules, and benefit timing can still create complexity.

Currency exposure

Retirees receiving pensions or investment income in foreign currencies face ongoing FX volatility risk.

Administrative fragmentation

Without employer support, retirees must personally manage interactions with multiple administrative systems, including My Number-linked filings, tax reporting, residence registration updates, visa renewal and benefit eligibility documentation.

Loss of social structure

Leaving the workforce often removes daily routines and workplace social networks. Without alternative social engagement, retirees may face declining physical activity, cognitive risks, and social isolation.

Stability Phase – Irreversible Decisions Checklist

Core Questions

Is your healthcare access secure, including enrollment health insurance and access to primary care and specialists?

Does your portfolio withdrawal strategy reflect conservative longevity assumptions ?

Is your tax residency aligned with how you actually live, particularly in managing global income reporting and avoiding double taxation?

Strategic Decisions in the Stability Phase

The Stability phase is where many retirees realize that planning focused on a retirement date did not adequately prepare them for retirement duration.

4. Phase 3 – Dependency

When Independence Becomes a Designed Asset

When: Advanced aging or health decline

Primary Risk: Governance vacuum

Dependency is often treated as an unfortunate possibility rather than a predictable stage.

Yet longevity data makes this phase statistically relevant. A retirement beginning at 60 may span 25–30 years. The final 5–10 years often involve some degree of care coordination.

Cross-Border Specific Risks in Dependency

Care system navigation

Japan’s Long-Term Care Insurance system (Kaigo Hoken) provides structured support beginning at age 65, however, initial application, eligibility assessments, municipal administration, and care coordination can be time consuming —particularly for foreign residents unfamiliar with local procedures.

Language and documentation barriers

Medical documentation, consent forms, and care planning discussions are often conducted primarily in Japanese. Cultural expectations around family roles and medical decisions can also differ, making preparation and clear communication essential.

Cross-border family coordination

Family members responsible for decision-making may live in other countries, creating logistical difficulties for medical consent, care supervision, and administrative procedures.

Liquidity pressure

Long-term care expenses may require liquid assets, which can conflict with retirement portfolios designed for long-term investment horizons.

Dependency Phase – Irreversible Decisions Checklist

Core Questions

Who has legal authority to act if you become unable to make decisions?

Where are your medical records and critical documents stored, and who can access them?

Is your chosen residence location compatible with realistic long-term care options? Or assisted living or nursing home need to be evaluated ?

Have you modeled financial scenarios involving long-term care needs?

Strategic Decisions in Dependency phase

Related article

Caring for Aging Parents in Japan from Overseas: What’s Realistic and How to Prepare

Japan Power of Attorney & Guardianship for Seniors: Overseas Families Need to Know Before a Crisis

Senior Care in Japan: Costs, Choices, and What Foreigners Should Know

Many retirees plan carefully for their active retirement years but neglect structured dependency planning. The consequences are rarely only financial—they often become emotional and administrative burdens for family members.

5.Phase 4 – Legacy

Cross-Border Execution, Not Just Inheritance

When: Late life and post-death

Primary Risk: Administrative burden across jurisdictions

Legacy planning is often framed primarily as tax optimization. In cross-border lives, however, the greater challenge is execution complexity.

Assets may be held across multiple countries, legal systems may apply different inheritance rules, and heirs may be required to navigate unfamiliar administrative procedures. The central question therefore shifts from how much is inherited to how easily the inheritance can be administered.

Cross-Border Specific Risks in Legacy

Asset fragmentation

Assets held across multiple countries—such as real estate, retirement accounts, or brokerage investments—may require heirs to navigate multiple legal and administrative systems simultaneously during estate settlement.

Conflicting inheritance frameworks

Different countries may apply different inheritance rules, including forced heirship laws, probate procedures, and marital property regimes.

Tax residency at death

Inheritance taxation and reporting obligations may depend on the tax residency of the deceased, the heirs, or both,potentially creating obligations in multiple jurisdictions.

Documentation accessibility

Critical documents—such as wills, beneficiary designations, financial account records, and property titles—may be difficult for heirs to locate or access, particularly when they live in another country.

Legacy Phase – Irreversible Decisions Checklist

Core Questions

Are asset titles and beneficiary designations aligned with your intended estate distribution?

Have you clarified which country’s inheritance laws will govern your estate?

Is key documentation organized and accessible to heirs, including wills, account records, and property documentation?

Would your heirs be able to navigate the estate administration process without significant legal or logistical obstacles?

Strategic Decisions in Legacy phase

Legacy is not the end of retirement planning. It is its final accountability test.

The true measure of a well-designed legacy plan is not only the value transferred—but how easily the next generation can carry it forward.

6.HR Sidebar

From my experience in global HR leadership, many employees delay retirement planning amid current duties. Yet retirement can span 20–30 years—a new life stage, not an end.In Japanese firms, late-career paths often emerge by the late 40s: executives may become independent directors or auditors; others shift to re-employment until 65. Post-60 transitions hinge on early preparation.

Real Story

One employee in his late 40s saw limited board prospects and likely affiliate transfer at 50. Interested in labor issues, he pursued the Certified Social Insurance and Labor Consultant (社労士) qualification while employed. When transfer came, he declined, launched his own firm, and built a stable business. Early planning transformed a forced change into opportunity—today his practice thrives as peers near retirement.

What Organizations Can Do

Effective transition programs (from companies or government) include:

Clarifying post-role accountability and smooth handovers.

Offering re-skilling beyond finance—covering healthcare, identity shifts, long-term planning.

Providing realistic late-career options: re-employment, advisory roles, second-career prep.

Addressing identity and network loss risks.

Structured transitions protect individuals and organizations. Government supports include Tokyo's Senior Employment Support Project (workshops, job matching, trial placements for 50+) and MHLW's vocational training/re-employment initiatives for job changers and seniors.

7.Wrap up

A cross-border life need not be complicated—if institutional systems are understood early. Without preparation, unexpected hurdles create unnecessary financial and emotional stress. I've seen many foreigners retire successfully in both the US and Japan. Their common trait: early planning and treating retirement as a structured transition, not a single event.

Retirement is a long journey through mobility, stability, dependency, and legacy phases. Recognizing them early gives you greater control.

Share your experiences or insights in the comments below.

If this article helped, please share it with friends, family, or colleagues planning cross-border futures.

Related article

The Retirement Checklist for Japan (2026 Edition)

Senior Care in Japan: Costs, Choices, and What Foreigners Should Know